Wise Plc (Ticker: WISE)

A compounder with attractive characteristics

Introduction

There are not many businesses out there which have these favorable characteristics as Wise have. Especially not at the stage of the company life cycle. Successful and well known investor within the community, Nick Sleep, called it ‘Scale Economies Shared’ (hereafter SES)1, where a company’s scale is shared with its customers in terms of lower prices. Well known companies which run through these principles are Costco and Amazon. It is not a coincidence that both have been highly successful businesses and profitable investments if you spotted them early on. In one of Nick Sleep’s letter, he explains SES:

“Most companies pursue scale efficiencies, but few share them. It’s the sharing that makes the model so powerful. But in the center of the model is a paradox: the company grows through giving more back. We often ask companies what they would do with windfall profits, and most spend it on something or other, or return the cash to shareholders. Almost no one replies give it back to customers – how would that go down with Wall Street? That is why competing with Costco is so hard to do. The firm is not interested in today’s static assessment of performance. It is managing the business as if to raise the probability of long-term success.”

Scale economies shared is not restricted to retail, you can apply it also into other industries. One of them is into fintech. Wise is a UK listed cross border money transfer business and was founded in ‘11 by two Estonians, Kristo Kaarmann and Taavet Hinrikus. Taavet left Wise in ‘21 to pursue political ambitions in Estonia while Kristo remained as CEO to run the company. Both have a decent amount of skin in the game.

Wise is a founder-led business, has a growing moat coupled with a ROIC of >20% and has still a long runway ahead (currently, market share below 1%). We believe Wise has a winning business model where any incremental savings are passed on to the consumer reinforcing its competitive edge. Wise is a compounder. It has similarities with one of our other investments, Adyen, and one fun fact about Wise, Adyen’s Co-CEO Ingo Uytdehaage is since ‘21 in the board of Directors at Wise. In the next sections we will break down Wise's business model and its competitive edge, then we will follow with the dynamics of the market it operates in. We will conclude this piece with some of the historic financials and corresponding valuation. An investment case is not complete without potential risks attached to it, so we will list those as well.

The Wise story

To explain what Wise does, it is best to explain how Wise started. Two Estonians, Taavet and Kristo, both worked in London. Taavet worked for Skype, while Kristo worked for Deloitte. Taavet, who lived in London, got paid in euros. Kristo who also lived in London and got paid in pounds. But he had a mortgage in euros back in Estonia. They both moved their money with their banks - which had expensive fees and bad exchange rates. They knew there had to be a better way. So they put their heads together and invented a beautifully simple workaround. Each month, they looked up the mid-market exchange rate. Taavet put his euros into Kristo’s Estonian bank account, and Kristo topped up Taavet’s UK account with his pounds. Both got the currency they needed almost instantly, and neither paid an extra cent on bad exchange rates or unreasonable charges. And this is how the Wise journey unfolded.

Wise went public in ‘21 via a direct listing on the FTSE. As opposed to a normal IPO, with a direct listing, no new money is raised. Wise didn’t need new money to grow further. It allowed current shareholders to monetize on the investment (think of PE’s, VCs) and for the company to get recognition. Today Wise is operational in 80 countries, has about 13m customers with a cross-border volume of £104.5m as per latest annual filings. Wise is a regulated business with 65 (country) licenses worldwide. In the UK, for example, Wise is labeled an Electronic Money Institution (EMI) authorized by the Financial Conduct Authority (FCA).

Business model

To explain the business model of Wise as simply as possible, let’s go back to our example of how Wise has started. Basically two people with both a bank account in the UK and in Estonia did a currency exchange by first deciding what the midpoint was of the EUR/GBP exchange rate and second, to transfer the money locally. So to do this ‘cross-border’ transaction, you need to know the exchange rate and both individuals need to have enough money on their account to be able to transfer it locally. Now if we scale this operation over 80 countries and multiple Wise accounts linked to a local bank account then hopefully you get the idea of what Wise does. Wise takes a very small fee, about 60bps on average for every transaction. The competition, mostly traditional banks, ask at least 10x higher fees.

You would ask yourself, why is Wise so much cheaper than traditional banks? This is because Wise has found a way to actually not move money cross-border. The money moves locally which is much cheaper. To invert the question, maybe it is better to explain why banking internationally is so expensive. To answer this question, we need to explain how banking in general works (which is called correspondent banking). If you want to send money (e.g £100) from your Barclays account to your friend who has a Natwest account, both UK banks, there are a few steps needed to make this happen. First Barclays needs to notify Natwest that you want to send money to your friend. The payer’s and payee’s bank exchange payment details and reconcile funds. This is called clearing. Then settlement has to take place, where is the process of actually transferring the funds from your account to your friends account.

If you bank with Bank A in the UK and want to send money to a bank in Japan, Bank D, there is often a chain of several banks - from A to B to C to D - who are all connected to each other. They then use SWIFT2 to exchange the clearing messages and local payment systems (e.g. SEPA) to settle debts between themselves. Sometimes the chains can get quite long with many banks in them, and the longer the chain is, the more expensive your cross-border payment will be.

Wise has since ‘11 built a network where they are connected with local banks and have funds with these local banks to do cross-border transactions locally. Wise itself is not a bank, it doesn’t have a Wise banking account (and it can’t pay interest on funds, will go later into this), but it is as close as it can get to be a bank. Because Wise bypasses the cross-border system and uses its own network, it is able to transfer money much cheaper. The more customers have an account with WIse and the larger the ‘cross-border’ volume, the cheaper and faster it can offer its service and the more valuable it becomes for customers. Wise reinvests its profits back into the business to improve its infrastructure and lower the fees. Scale economies shared (SES) is a business strategy where companies share their cost savings with customers through lower prices. The goal is to gain market share and create a virtuous cycle where customers transact more, which allows the company to save more costs and pass them on to customers again. This resonates well with the Wise customers, because 2/3 of the new customers come via worth-of-mouth.

Ambition

Management is very clear about its ambition. They want to move trillions in cross-border volume and continue to strengthen its infrastructure and lower its prices. They want ‘evangelical customers’, a term they often use during the earnings calls by ‘wowing’ the customers. They know a superior and cheap service will get them to their goal. Their business model is similar to that of Costco or Amazon as both share profits with their customers . There is just a tremendous obsession about the customers and a relentless focus on doing this specific thing very well.

Wise serves retail customers and small- and medium-sized businesses via its Wise Account product and Wise Business account product. For banks or large enterprises, who want to enjoy lower costs and faster transactions, Wise is offering the Wise Platform. Wise Platform connects to banks via an API and gets them off the SWIFT network into their own platform, which we described earlier is much more efficient.

Wise Platform

The Wise Platform gives banks the option to create a better and cheaper service for their customers. Wise platform is a white label product that connects its payments infrastructure to banks which in turn can give the Wise product to its own customers. The banks can decide how they want to market it to its customers. Customers don’t even have to know its Wise who handles the cross-border transaction. A lot of neo-banks like Monzo, Bunq and Nubank are connected to Wise. But recently also larger banks like Standard Chartered and Morgan Stanley have joined Wise. You would ask yourself, why would a traditional join? This was asked in the FY23 call. This is what the CEO had to say about it:

“I know the Wise platform, I think there's no specific catalyst and then there's two groups that Harsh mentioned which were -- we see more traditional banks, especially starting in Asia, I guess they're slightly faster moving. So for banks it's always hard and slow. So we see the Asian banks actually go faster, the Shinhan Bank, the Mandiri et cetera. And we see the US challenger banks are -- generally challenger banks go faster as well in the Wise Platform adoption. I think one of the catalysts I just wanted to add to that is, as the kind of the years go by, banks do see their customers using Wise and for them it's increasingly valuable to bring these customers back to their own platform, which is their own apps, which is what we're supporting with Wise Platform. So the logic for our bank partners a lot is they see the customers using the benefit of Wise and they would rather -- much rather, and we would much rather them have that in their own apps.” (Kristo Kaarmann, CEO)

Offering this product to banks is pretty smart. By firstly counter positioning Wise as a solution to a complex cross-border problem, with banks unable to compete due to their cumbersome legacy IT systems, it offers them a solution with the Wise Platform. If banks want to give their customers the best possible and cheaper service, they will work with Wise. The opportunity of the Wise Platform is massive. If more banks partner up with Wise, that would be the bull case. The CTO Harsh Sinha received a question about this in the FY24 call:

“And then secondly, on the Wise Platform. So Harsh, you mentioned Swift, you also mentioned Nubank, which I think has about 100 million customers in total, and it's growing tremendously. How should we be thinking about the sort of opportunity there? When are we going to start seeing sort of the effects coming through? Thanks.” (Analyst)

So to give a bit of context to the question. Wise recently onboarded a large neo-bank in Brazil, Nubank.

“Yes, for Wise Platform, so first of all, we are excited that we have now 85 partners globally, who think what we've built over the last 13 years can be used for their customers, right? So, this is testament to what we've invested in over the long term. I can tell you like even four, five years ago, when we went to the banks, they'd be like, oh, I'm not sure. And now they're seeing that change and they're seeing it, because their customers are moving to Wise and they're figuring out how to retain these customers in their own experience. So, that's great. Specifically, on Nubank, like, yes, it's a flagship bank there now in LatAm and it's still early days, as we just launched the integration. But I have to remind you that the challenge that our Wise Platform team has is that the core business, as in like the people, who come to wise.com and our Wise apps, that's still growing pretty healthily and very healthily. So, as a percentage basis of what volume moves across partners, it's still early days, right?” (Harsh Sinha, CTO Wise)

“But I fundamentally believe and we fundamentally believe, again, this is a much more longer-term investment, because if you think about it from a bank's customer perspective, if the banks are doing the right thing for the customers, they should be plugging in the cheapest, best infrastructure into their own apps. And we are seeing this with the neobanks, because they are faster to move. They may not have old relationships, correspondence. So that's, they're seeing that and that's becoming an advantage for them that the incumbent banks are trying to defend against. So, still early days for Wise Platform, but overall, we're very excited about what's happening.” (Harsh Sinha, CTO Wise)

Market and competition

The cross border payment market was $190 trillion in ‘23 and is expected to grow with a CAGR of 5-6% due to globalization. The market Wise is focussing on is a subset of this $190 trillion. Currently they focus on the retail and SMB market, which according to them is about £14 trillion, where retail transactions accounts for £2 trillion and transactions done by SMB accounts for £12 trillion. Wise has a market share of 5% for the first market and less than 1% for the second market. Another market they are tapping (via Wise Platform) is the money moved by large enterprises (£13 trillion).

So the cross-border payments market is massive by itself. The majority of these payments are done by banks, which is about 2/3. Then about 10-20% is done by money transfer operators like Western Union and MoneyGram. The rest is split up by other players like Wise, Revolut, Remitly and more.

Banks ask very high fees and there is even regulatory pressure to get it down. According to the World Bank, the global average cost of sending $200 from one country to another is about $12.50 in the ‘23 or 6.25%. The UN has set a target that cross-border transfer fees should be not more than 3% with no corridors higher than 5%. People who are actually suffering are normally immigrants, trying to work overseas and transfer money back every month to support their families. Regulatory pressure makes sense and plays into the benefit of Wise, which is charging currency just 0.59% on average in fees (10x cheaper than global average).

So to go a bit more into detail regarding the players active other than the traditional banks, you have

MoneyGram and Western Union: Western Union is the most familiar and longer one and has been around for a while. They have about 500,000 agent locations in over 200 countries. Customers can send money by phone through the Western Union website or in person. Costs vary per transaction, but you can imagine the fact they have 500,000 agent locations, they never can be as cheap as ~60bps.

Digital money transfer services: on top of the ‘old’ money transfer services, you also have players like Rimitly (listed), OFX, Instarem, Xoom (PayPal) which run the same business model as WU and MoneyGram but are digital and hence can offer more competitive fees. Still they actually transfer money and take a small bid/offer charge on the FX

Revolut: the most serious competitor if you ask me. Revolut is a UK based neo-bank with about 45m customers. Currency exchange is not their core product like it is for Wise. They offer extremely competitive fees, subsidizing even to keep you on board as a customer. On the weekends, the fees are significantly higher though.Eventually the customer needs to use other banking products from Revolut, otherwise the cross-border transactions will never be profitable for them. I am myself a customer of Revolut and use it to exchange and send money from £ into €. I pay a small subscription (£7 p/m) for this, but I am not using any other services from Revolut. Probably I am not their desired customer

Below you will find a graph of monthly active users (MAU) since October ‘24

Moat

Wise has a couple of moats. Let’s start with the most important one: their scale and low cost. Due to the fact they actually bypass cross-border transactions, they benefit from lower cost. The more customers they have and the more volume they do, the lower they can set their fee and the stronger the moat becomes. Wise managed to reduce fees this year from 67bps to 53bps. This to me is a confirmation of a widening moat. Wise benefits from flywheel where, comparable to the early days of Costco and Amazon, ‘scale economy shared’ which is an extremely durable competitive advantage.

Wise also has a technology advantage. Everything is built in-house and they employ about 800 engineers, which is one of the largest engineering teams in the world working on the problem with cross-border payments. They relentlessly focus on this one problem and try to improve it day in day out.

Regulatory moat. We didn’t touch upon the number of local payment systems Wise is currently on, but this is extremely difficult to realize. Also the licenses it needs to obtain to operate in a country can take years. They have 65 licenses and for any new entrant, it will mean they have at least a decade of head start. A former Bank Partnership Executive at Wise explained a bit the process of obtaining a license in a country:

“Once you're in the licensing process, you're juggling many things simultaneously. In the final stretch, the last six months, it takes about six months to integrate with the banks. Everyone says about three months, but in my experience, it's about six months. There are three stages, even with the banks. First, you get the approval to open the account, which is conditional on your license. Once that approval is given, there's a whole application process to physically open the account. It makes no sense to me, but it's a separate process. So, there's an agreement to work with the bank. Then, once you get your license, you have an account opening process. The integration is only subsequent to the accounts being opened because, to integrate, you need to have the accounts for user acceptance testing. You need real accounts to send dummy transactions to ensure everything works. The technology part could be quick if you have the right resources on both sides, the bank and the company. It could take two to three months.” (Former Executive at Wise, ‘24)

Management and culture

Founder led business, the founder /CEO has 18% of ownership. His co-founder who left to pursue political ambitions in Estonia, also still owns about 5% of the shares. CEO, Kristo Kaarmann, takes a small salary and has no extra compensation in terms of share options. Other senior management have decent skin in the game as well so interests are well aligned with shareholders.

The board of directors is extremely strong with members like:

David Wells: Independent non-executive chair and former CFO of Netflix

Hooi Ling Tan: Independent non-executive director and co-founder of Grab

Ingo Uytdehaage: Independent non-executive director and Co-CEO at Adyen

We met management in April ‘25 in London when they hosted their first investors day. They called it Owners Day, which resembles well how management thinks about their shareholders and the business.

The culture is open, the management team is relatively young and I felt each of them had a tremendous amount of experience in their own field, but were all aligned in their relentless focus on the customer. Kristo, himself is only 44 years old.

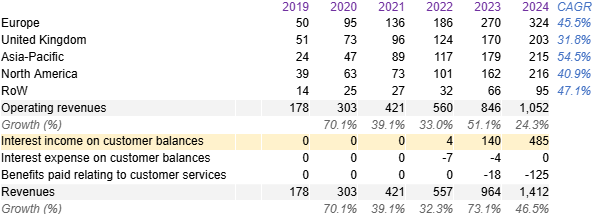

Financials and capital allocation

Wise has a sound balance sheet and is extremely profitable for the growth stage they are in. The gross margin is about 60-70% and they spend about 20% on marketing and 20% on R&D and let the rest flow to the bottom line. About 2/3 of the customers come from word-of-mouth. This is a result of the investments they do to make the product better and lowering fees. The ROIC is high, above 20%. That is not surprising if 2/3 of growth is without any marketing spending. There is some capital spent on share buybacks to keep tackle the share dilution from stock based compensation. SBC is about 5% of revenues so manageable. Especially for a fintech company which is growing about 20-30% a year.

Recent years, Wise receives quite a bit of income from interests due to its high cash balances. Customers tend to leave money on their Wise account. Currently WIse has about £10bn of cash on their balance sheet. As it is not a bank, they are not allowed to pay customers interest. They are trying to find ways to pay the customers back. For now they use a great proportion of the money to reinvest in the product (and hence be able to give lower fees). The income is real and a nice problem to have. Management expects to keep profitability around 20% of revenues in the medium term. But if at some point growth stalls and there is no room to reinvest the profits, margins can easily increase.

As take rates on cross-border transactions decrease, the fact that Wise offers customers more services, they manage to slowly increase the fees from these services. The bold ambition from management to bring cross-border fees towards zero becomes more of a viable business model as ‘other fees’ are growing.

Risks and opportunities

If banks find a way to create a better payment system (like SEPA in Europe) globally. This might be hard to imagine now if you see how complex and cumbersome the payment system is, but countries are trying to make things better. For example, India and Singapore made in Feb ‘23 cross border payments in realtime using the Unified Payments Interface (UPI) and Paynow

Stablecoins - cryptocurrency is for the last couple of years a hype amongst investors, but the technology behind it could be a threat for Wise. I

Visa/Mastercard have a whole infrastructure between banks and they are trying to get a foothold in the cross-border payments market. In ‘21 Visa acquired for example Currencycloud - a global platform that enables banks and fintechs to provide innovative FX solutions.

Reputational risk - Wise operates in a highly regulated environment where it might be harder to monitor illegal transactions like terrorist financing, money laundering etc. Being fined and exposed van hurt reputation

Adding traditional banks to the Wise network via Wise Platform and adding larger enterprises. This is a massive opportunity because Wise could scale very quickly if larger banks partner up with Wise

Higher cash balances from customers on Wise accounts which will result in higher interest revenues

Becoming a bank (although would result in more compliance costs) and be able to offer more products and services to its customers

Long period of high interest rates could give a continuous boost to the free cash flow

To keep track if Wise remains on track to compound, we would monitor the following KPI’s

Track cross border volume (ideally grow annually by at least 20%)

Monitor onboarding of traditional / larger banks via Wise Platform

Monitor the cross-border fees Wise is giving its customers. The lower the fees, the stronger the moat

Redeployment of the FCF, if less deployed, means growth opportunities are shrinking

Conclusion

Wise is an extremely attractive business to invest in. It has all the characteristics we look for in a business. It has a small market cap, so not investable for larger / well known investors. As it is listed on the FTSE 100, it is a bit under the radar. As a small investor we can benefit from this. Adyen is for example about 5x the market cap of Wise. As the total addressable market is large and Wise is able to grow fast and take market share from competitors, I see a bright future for the company. The market is benefitting from favorable trends with a CAGR of about 5-6% the coming years. The fact that management laser focuses on the customer, wanting to have ‘evangelical customers’ resonates with me.

Disclaimer

The information in this article is provided for informational and educational purposes only. The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence. None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions.

https://igyfoundation.org.uk/wp-content/uploads/2021/03/Full_Collection_Nomad_Letters_.pdf

SWIFT stands for the Society for Worldwide Interbank Financial Telecommunication. SWIFT provides a secure network that allows more than 10,000 financial institutions in 212 different countries to send and receive information about financial transactions to each other. Before the SWIFT network was put in place, banks and financial institutions relied on a system called TELEX to make money transfers. TELEX was slow, and the system lacked the security necessary for a time when technology was making rapid progress.

Excellent and very detailed! I don’t think stablecoins are an immediate threat and even if they gain traction this might allow Wise to enable it’s own stablecoin based cross border solution for when it has imbalances between xccy flow interest.

Thanks for sharing🙏 Sounds like a true long term compounder.