A discount retailer wrapped in a P/E firm

A steady compounder with plenty of runway left...

For our portfolio we look for compounders, companies who can grow their capital at attractive returns for a very long period. When we find such a company, we try to invest in them at attractive valuations and run this investment for at least 5 to 10 years, or longer.

A company that gained our attention is 3i Group plc or 3i (ticker: III). The company was founded in ‘45 in the UK, but really started to change its course when Simon Borrows became CEO in ‘12. Initially 3i is a private equity firm, which typically attracts external capital to grow their assets. Since ‘12 3i stopped to attract external capital and used their own capital (and balance sheet) for their investments. Also they have an odd characteristic as a private equity, where they tend to keep their ‘winners’ in their portfolio permanently. One of these ‘winners’, is their majority stake in Dutch low cost retailer Action. 3i invested in ‘11 for £106m in Action and since then the value of this investment went up more than 150x. Also the cumulative returns in terms of dividends has been more than 25x their initial investment, as total distributions totaled about ~£2.8bn. Action is unique and 3i realised this early on by keeping this stake and if or when possible, increasing it. Currently 3i has 57.9% stake in Action. Action consists of about 70% of the total portfolio value. 3i is also known for its investment in Basic Fit in ‘13 where it still owns 6.7% of total shares.

Action - introduction

Action is already 30yrs in business, but growth really started to take shape when 3i got involved. Most of us know Action, but the ones who don’t know them, they are a low budget retailer. Action sells ~6,000 SKUs divided over 14 categories: food & drink, DIY, stationery & hobby, household goods, laundry & cleaning, personal care, garden & outdoor, toys & entertainment, pets, decoration, linen, clothing, health and multimedia. And ⅓ of the assortment is fixed and the other ⅔ is not. Every week Action has 150-200 new articles in their store creating a treasure-hunt type of shopping experience for customers. About 70% of their products (i.e. primary offering) is below €2. Action has A-brands, supplier brands and private labels.

From ‘12, the expansion towards other countries started to accelerate further. Action is the fastest growing non-food discount retail of Europe and currently has 14m customers every week.

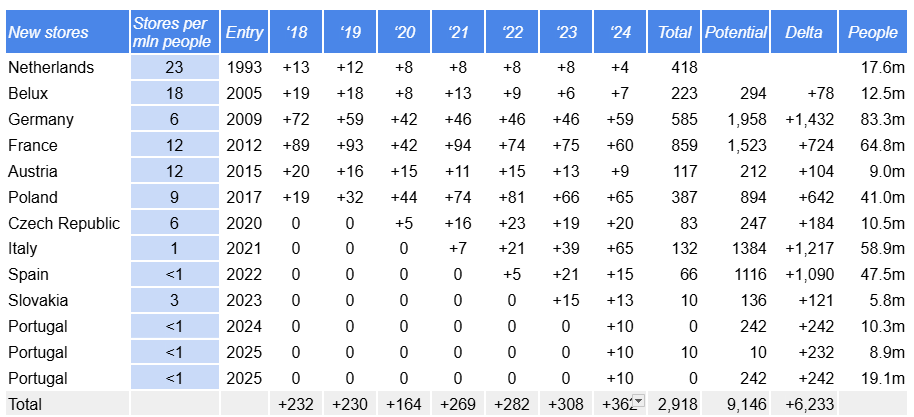

The latest financials show that Action’s sales were €13,784m (+22% yoy) and EBITDA of €2,076m (+29% yoy). What makes Action so special is their very cost efficient way of running the business, their prudent approach in expanding and their ongoing customer obsession. As of March ‘25, Action has 2,918 stores open spread over Europe. The ease they can open successfully new stores in different countries amazes me. I have been doing extensive research to find out why and how this is possible. I came up with the following answers:

With their format, they don’t face direct competition. They change most of their assortment frequently. Also it seems that it doesn't matter in which country Action is operating, customers love their products. The assortment per country is the same

Strong culture with the CEO Hajir Hajji being for decades and holding various positions within Action before becoming CEO. The combination with 3i’s management team to optimize capital allocation works extremely well

Flywheel effect where they become bigger and bigger, they can source cheaper (economies of scale) and have bargaining power and pass on these prices towards their customers which keep happy customers to return

Long potential runway

Since ‘18 Action have been expanding their footprint in new countries while cementing their presence in their core countries. Since Action so easily expands, it would be interesting to see what the potential is. Based on 23.5 stores per 1mln people, in the current countries, Action could grow to ~8,500 stores, or more than triple the current number of stores.1 The only question is, will this potential runway in any way be disrupted? Could be, but Action already has a presence in these countries. It built brand recognition. If they manage to continue to grow without interruptions, we have a pretty decent investment case here. Let’s say 8,000 stores times €4.7m (avg revenue per mature store), we end up with €38bn in revenues (from €13.8bn in ‘24). If we assume 370 new store openings (management guidance upcoming 3yrs), Action could grow for another 15yrs. Management estimates themselves there is a white space of ca. 5,000 stores. We think that they are a bit conservative in their estimates, but nevertheless, even if we are off by 1,000 stores, it must be clear that the runway is there.

Business model

Action opens 1,000m2 stores tier 2 or tier 3 locations. The products are almost 2x cheaper than its competitors and products are sourced from China (49%), Europe (45%) and rest of Asia (6%). In more detail, Action works with 686 suppliers divided over 53 countries. Action stores are stocked from the DC’s which are spread all over Europe: NL (2), Germany (2), France (5), Poland (4), Slovakia (1). And in ‘24 new DC’s will be opened in Spain (1), Italy (1) and ‘25 a DC will be opened in Germany (1). There are 3 hubs in Europe: Le Havre and Saint-Martin-de-Crau (FR) and Wroclaw (PL).

Store economics / ROIC

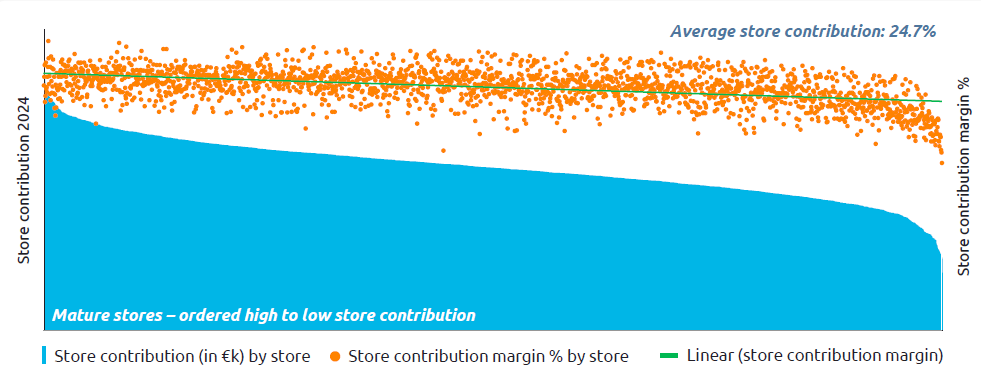

The economics of a newly opened store are highly attractive. The upfront capex is €0.5m, after 7 months the store reaches break even and beyond that it becomes profitable. The store contribution, which is gross margin less direct opex would be in less than 1yr about €0.7m. Difficult to exactly calculate the ROIC but with the available information , we estimate it to be around 100%.

Competition

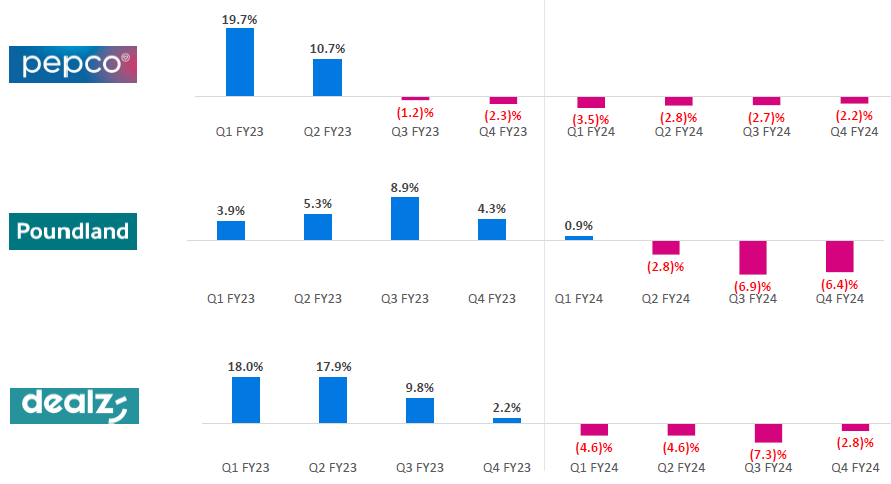

Action operates in a market which is in between apparel/homeware discounters and grocery/FMCG. Action overlaps both markets and hence doesn’t have many competitors. Below we pasted a competitive landscape we found in one of the investor presentations of competitor Pepco.

Although the assortment does not overlap 100%, the closest competitors of Action are Pepco and Tedi. Still Action is in terms of revenues larger than #2 and #3 combined.

Pepco

Pepco is listed and operates about 5,000 stores in mainly CEE and the UK under the names Poundland, Dealz and Pepco. It has about €5-6bn in revenues and profit margin of ~5%. Pepco offers, like Action, a diverse range of FMCG, homeware-led GM products. But it differs from Action as it also offers apparel. Although this has higher gross margins, it is more competitive from as prices are high enough to sell online (i.e. Shein). Also it has higher lead times. Pepco states that they are offering about 250 new products per week. Poundland has ~800 stores in the UK. In Poland, Pepco has about ~1,400 stores. Pepco is growing its store base with on average 400 per year, mainly in CEE and Italy and Spain. In CEE, the environment is less competitive.

Circa 60% of products are sourced out of China and 25% from Bangladesh. As a large portion of their products are coming from Asia, the business model is pretty fragile and any disruptions in the supply chain can hurt performance. It happened this year and affected results. When comparing prices on food products, it is pretty similar to the prices of Action. Majority of sales are however clothing. If they wouldn’t sell clothing, I think Pepco would be a more serious competitor to Action.

In the last couple of years, Pepco group suffered from competition and LFL sales have dropped the last couple of years due to deflation and intense competition:

Especially Poundland is struggling and according to the latest headlines, Pepco is trying to sell Poundland. Some PE firms seem interested.

TeDi - German non-food discount retailer

German non-food retailer. Non-listed. Founded in early ‘00s with in ‘04 120 stores. And since then gradually expanded in Germany and from ‘11 outside Germany. Currently has 3,200 stores (more than Action) with about 2,000 stores in Germany and the rest outside Germany. Categories are: party & gift wrapping, home decoration, crafts & DIY, writing, household, cleaning / white label, drugs / cosmetics, accessoires, outdoor & leisure, pet supplies, toys. Has the ambition to grow towards 5,000 stores (set this ambition in ‘21). Doesn’t have brands. Requirement profile for expansion:

Location: Downtown A or good B location. District location with high frequency of casual customers, row of specialised stores, shopping centres, foyer zones in self-service stores, or an individual location

Trade environment: Foodstuff discounters, consumer markets, textile and shoe stores, drugstores

Commuting area: more than 20,000 residents at hub or over 20,000 residents in the commuting area

Surface area profile: at least 550m2 selling space + ca. 50m auxiliary areas, pedestrian precincts or location with high consumer frequency over 300m2 selling space, depending on the trade environment up to 1,500m2 selling space is possible

Operational in 15 countries. Typically avoided direct competition with Action:

No stores in the Netherlands

Recently expanded in other core countries of Action (i.e. France, Belgium)

Management

I consider management as strong and a key differentiator to the success of Action. The combination of expertise coming from 3i on the capital allocation side and business know-how from CEO and CFO at Action works well. The current CEO Hajir Hajji has been within the firm for more than 25 years and held various senior positions within Action. As such, I think she has a good and complete understanding of the business. It is not disclosed if she has any insider ownership, but she does operate like an owner. Simon Burrows is the CEO of 3i and has about £500m in capital tight to 3i. His interests are aligned with shareholders. He made the important decision to keep Action as a long term investment.

Moat

Action enjoys a durable competitive advantage due to a couple of key differentiators:

It is a low cost operator with a lean structure, low cost profile (i.e. limited marketing, tier 2 or tier 3 locations) and due to its scale as the largest low cost retailer in Europe, it can negotiate lower prices and increase margins over time or pass these savings on to customers

Strong culture with management for decades involved in the business. Flat culture, no nonsense mentality and frugal

Difficult to copy the business as Action doesn’t only differentiate on price. It makes sure that the assortment changes constantly. Every week 150 new products. Customers can expect every time when visiting Action, ‘an element of surprise’

Strong brand equity

Financials

Over the lastt 10 years, Action grew the number of stores with a CAGR of ~20% while like-for-like grew since 3i stepped in on average 8%. Sales per store grew from €2.93m in ‘14 to €4.72m in ‘24. As 3i keeps paying itself a dividend, leverage ticked up to an elevated level of 2.6x. As the EBITDA continues to grow, leverage should come down again, but 3i will keep paying itself a dividend so expect leverage to remain above 2x for the foreseeable future.

The gross margin of Action is impressive considering it is a retailer and is round 40%. Almost all product categories are at (or higher than) a gross margin of 40%

Which makes all mature stores profitable!

Valuation

It is not easy to value 3i or Action as you have to keep into account a couple of important factors:

Increasing proportion of Action’s value in the 3i portfolio over time

Stake of 3i in Action which increases over time (from 43% in ‘19 to 57.9% currently)

Action uses the EV / EBITDA multiple as a valuation metric (of 18.5x). As the leverage (currently) is high, we rather look at P/E multiple.

Take into account different currencies (£ / €)

Valuation Action on “standalone” basis

We will start with Action and try to get an idea what the company would be worth by itself in 5 years time. Key drivers for Action’s revenue growth are 1) number of new stores opened and 2) like-for-like sales growth. For the coming 5 years I forecast a LFL growth of between 6% and 8% which is also in line with management expectations.

This year, Action expects to grow the number of stores with ca. 370. I expect the same store growth in the next 5 years.

Based on these variables, I expect revenues to grow from +22% in ‘25 towards +15% in ‘29. In ‘29 Action should be able to produce a profit margin of 10%. Based on this we expect the revenues to be in ‘29 around €31bn and net profit €3.1bn. Value of Action with a P/E multiple of 30x and £ / € of 1.20 is £75.7bn.

Proportion Action within 3i and estimated market cap Action

Currently 3i owns 57.9% of Action. And Action makes up ~70% of 3i’s portfolio value. Below you can see what proportion of the portfolio value contains from Action. It has been growing from 5% in ‘11 to 70% in ‘23. I expect this to gradually grow larger. In ‘29 I expect Action to be 80% of 3i’s portfolio value.

Market cap of 3i is currently £40.1bn and since Action comprises 70% of portfolio, the hypothetical market cap of Action is (70% x £40.1bn) £28.1bn. When we assume 100% equity, Action would be £48.5bn (£28.1bn divided by 57.9%). This would result in an IRR of 10.2%2. The dividend yield is 1.9%, you would reinvest the dividends, IRR could reach 12%.

3i’s valuation methodology regarding Action

3i uses the EV/EBITDA methodology to calculate the valuation of Action. They use a multiple of 18.5x. To convert this into P/E multiple, we have to subtract the debt from the EV and depreciation, interest and tax from the EBITDA to get a clean P/E multiple. If we look at the latest numbers FY24 numbers, 3i states the following:

Net sales: €13,781m

Operating EBITDA: €2,075m

Operating EBITDA margin: 15.1%

Run-rate EBITDA: €2,075m

Net debt (estimated): €3,966m

Net profit (estimated): €1,148

Equity value: €32,5563 (€38,388m - €5,832m)

P/E multiple: 28.4x

If we look at the P/E multiple currently, the market gives Action a NTM multiple of 40.6x, which looks high. If we calculate the P/E multiple of Action since ‘15, it has been between 30x and 40x.

What about the other holdings?

We could include the other holdings into our valuation, but if we assume to hold Action for a very long period, Action will be a very significant part of the holdings (currently 70%). In 5yrs we estimate about 80% of the portfolio would consist of Action and in 10yrs time, 90% of the portfolio could consist of Action.

Conclusion

Action is a very strong business. During this deep dive where we extensively analysed the business, its market and the competitors, I don’t have the impression Action can easily be disrupted. Action is a discount retailer, but enjoys strong brand equity. It is not just cheap, it offers a variety of assortment which by itself is constantly changing every week. Customers can ‘treasure hunt’ every week for new deals. The (non) food discount retailer market, by itself, has been growing rapidly. Both competitors TeDi and Pepco have been adding around 300-400 stores per year over the last couple of years. There seems to be room for all players to grow. Then your natural question is, who are they taking market share from? Is it the supermarkets? The smaller mom & pop shops? In the Netherlands, it has been clear who Action is taking market share from: Blokker, Bruna, Big Bazaar and most have been bankrupt. Big Bazaar, also a discount retailer, didn’t survive the competition with Action. In Poland, where Pepco is the larger and established player with 1,300 stores, Action is breaking through as they have added ~300 stores since ‘18. In Poland, according to the latest statements, Pepco seems to struggle this year, while Action continues to grow. Maybe too easy or too soon to say there is a direct relation, as Pepco also offers apparel, but will not rule out either that Action taking share from Pepco. In the next few years, this will become more clear. In Spain, both Action and Pepco go head to head and invest heavily in store expansion. Action seems to do better.

Like any investment, the return will be based on the durability of the growth. If Action will be able to open successfully about 350-400 stores for the next ten years, you will enjoy holding a piece of this business.

Risks

High leverage currently (2.6x net leverage) while exploiting potentially the business too much

Potential threats from Amazon, Temu. Change in consumer behaviour (i.e. buying more online vs offline)

If the CEO leaves, we don’t know if there is a good successor in place. 3i CEO Simon Burrows in his late 60s

Supply chain disruptions, tariffs

In the Netherlands, there are 23.8 stores per 1mln habitants

[(£75.7bn / £48.5bn)^(12/55)]-1

Equity = EV - (net) debt; EV = €2,075 x 18.5x = €38,388m & net debt (‘24) = €5,832