Topicus.com Inc (TOI)

Highly dislocated opportunity for the long-term investor

Capital compounding is all about finding exceptional compounders early in their journey and, when the investment thesis holds, partnering with them as long-term shareholders. This piece focuses on Topicus.com Inc. (TOI), which we believe is one of those rare compounders.

To understand Topicus effectively, we must first step back and examine its parent, Constellation Software (CSI). Topicus is not merely a European carbon copy of the world’s most successful serial acquirer; it is a unique hybrid created in 2021. The company was formed by merging one of CSI’s existing operating groups, Total Specific Solutions (TSS), with a separate Dutch software company called Topicus.com B.V. The combination was specifically designed to succeed in the European market, which is highly fragmented by diverse languages, laws, and cultures.

But this thesis does not exist in a vacuum. The context has shifted dramatically.

Mark Leonard stepped down as President on September 25, 2025. His departure was unexpected, and the timing—coming just one day after a conference call regarding the impact of Artificial Intelligence—sparked anxiety among investors. This uncertainty led to significant selling pressure, causing the share price to experience its largest drawdown in history and dragging down Topicus with it.

Currently, software companies are broadly perceived as being vulnerable to disruption by AI, and as a result, many are trading at steep discounts relative to their historical valuations. For the disciplined investor, this dislocation may be the window of opportunity we have been waiting for.

Table of Contents

Brief overview of Constellation Software

Mark Leonard

The CSI Playbook

The Five Key Metrics

Employee / shareholder alignment

Topicus.com Inc (TOI)

Topicus.com: The Rise of CSI 2.0

The ‘Hunter’ versus the ‘Builder’

Minority stake in Polish VMS serial acquirer Asseco

The Financial Logic: A Levered Yield Play

Sygnity Case Study: The Proof of Concept

The Moat of Topicus

The Proprietary Data Engine

The Benchmarking Machine

Structural Decentralization

The “Perpetual Owner” Advantage

Will AI disrupt Constellation and Topicus?

Financials and Valuation

Valuation

Current situation and the opportunity

The Capital Deployment Machine

The Recession “Call Option”

Conclusion + Model

Why we prefer Topicus over CSI

Brief overview of Constellation Software

Constellation Software (CSI) is the ultimate compounding machine, and Mark Leonard is the architect who built this exceptional business. CSI has successfully compounded free cash flow (FCF) with extremely high returns for decades. In 2007, FCF per share was $1.62; in the last twelve months (LTM) of 2025, it reached $79.93, resulting in a CAGR of ~25% over nearly 20 years.

“Growing organically while generating a high ROIC is, to my mind, the toughest task in the software business.” (Mark Leonard, CSI, 2014)

CSI is a perpetual buyer of mission-critical Vertical Market Software (VMS). The business is structured to scale acquisitions rapidly and is decentralized to perfection. Regarding CSI’s philosophy on autonomy, Mark Leonard wrote:

“As perpetual owners, we care about the long-term health of our many small businesses. We try to provide an environment in which they can flourish. The primary way we can do that is by making sure that they have high-quality managers who are compensated according to rational long-term oriented incentive programs. We make sure that BU managers have access to capital when they have opportunities. We try to foster a collegial environment so that best practices are shared. Late last year, when we reviewed our BU demographics, we had 243 separately managed BU’s, up from 193 the prior year. We currently see no fundamental limit to the number of BU’s that we can manage, but we are very worried about limits to the number of good VMS businesses that we will be able to buy at reasonable prices.” (Mark Leonard, CSI, 2018)

Mark Leonard not only pushed decision-making down to the local level but also ensured there was the utmost discipline to meet the 20% to 30% IRR hurdle rate when acquiring a business. This discipline is a valuable lesson for all investors:

“I recently worked on a large transaction. With every day that passed, I could feel my commitment to the process growing… not because the news was getting better, just because I was spending more time on the prospect. The investment didn’t quite meet our hurdle rate. We were not able to negotiate a structure that got us an extra couple of points of IRR, and the big one got away. The difference between investing and not, was tiny.” (CEO, Mark Leonard, 2017)

This discipline is not exclusive to Mark Leonard; it is embedded throughout the organization. Managers at the Business Unit (BU) level are empowered to deploy capital autonomously. This highly decentralized structure—combined with a strong culture of high-return capital deployment—is what makes CSI so successful.

“If a small investment with a borderline hurdle rate is proposed, we sometimes allow it to proceed. Our rationale is that if the investment goes sideways, then it becomes a ‘lesson’ for the Operating Group or BU personnel that proposed it. If the investment goes well, it becomes a ‘lesson’ for Bernie and me.” (CEO, Mark Leonard, 2017)

By diligently tracking post-acquisition performance, managers can assess what is working and where improvements are needed. The more deals CSI completes, the more data it has on what “good” looks like. Over time, this flywheel has become stronger and stronger.

Source: Capital Compounding

Above, I have plotted a simplified chart of the CSI organizational structure to illustrate how rigorously responsibilities are pushed down. This structure allows the organization to scale and execute 1,100+ M&A deals. Every Operating Group (e.g., Harris, Volaris) has its own CEO, and authority is further delegated to separate Business Units with their own managers. The ‘OpCos’ are the acquired companies themselves.

The CSI playbook

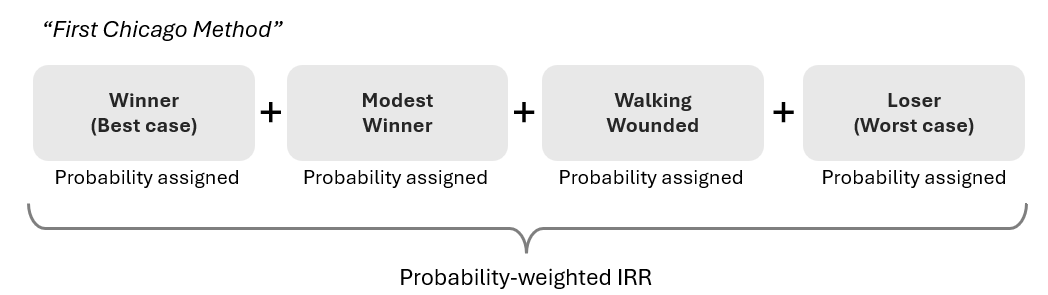

Pre-acquisition, CSI M&A executives build a 10-year DCF model with a constant terminal multiple. Each assumption is stress-tested against the 1,100+ historical acquisition data points within the group. Given that IRR is time-sensitive, the FCF in the early years drives the majority of the IRR target. This means right-sizing costs and repricing contracts immediately are crucial to hitting returns. CSI runs four scenarios, probability-weighted to estimate pre-tax FCF.

“There are three hurdle rates. Less than a million in revenue is 30% IRR; above four million, you can drop to 20%; and 25% is for everything in between. There is another hurdle rate of 15%, but that is on deals so large they’re not in CSI’s wheelhouse. Above 50 million, you can go to 15% but they might only do one of those per year. Dropping those thresholds by 2.5% won’t have much impact…if you don’t reach the hurdle rate, you can’t get a deal done. If we did all that work and modeled it out at 19%, the deal won’t get done. Playing devil’s advocate, if we bought a business at 17.5% IRR with four million revenue, and it allowed us to buy more companies, is that not a better result than doing nothing?” (Former M&A Director, CSI)

Source: Capital Compounding

This is how it looks like; it is a slight variation of the “First Chicago Method” which Mark Leonard probably used in its early days as a venture capitalist. The manager assigns the probabilities to each of the four scenarios to calculate a probability-weighted expected return (IRR) and estimated pre-tax FCF.

Because the IRR calculation is time-sensitive, the model places significant emphasis on FCF generated in the early years. Consequently, CSI focuses heavily on immediate post-acquisition levers—such as price increases and cost right-sizing—to ensure the “Walking Wounded” or base scenarios still meet return thresholds

The Five Key Metrics

CSI optimizes acquired businesses by immediately restructuring their P&L statements into a standardized format. This allows them to benchmark the new acquisition against data from their vast portfolio to identify inefficiencies. They break costs down into five specific buckets (R&D, S&M, Professional Services, Maintenance/Support, G&A) and apply rigorous ratios to ensure each department generates a sufficient return on investment. In the picture below I tried to visualize it to make it a bit more understandable.

Source: Capital Compounding

Because CSI owns so many VMS businesses, they can instantly spot if a target has “two too many Professional Services heads” or is underpricing its maintenance. They aggressively implement value-based pricing. If a product is mission-critical, has high switching costs, and low attrition (<5%), they will often raise prices significantly, as the software usually represents a small fraction of the customer’s total cost base.

Employee / shareholder alignment

Although CSI is not known to be a high paying employer, it made sure that the bonus structure was well aligned with long-term shareholder interest. There is a complicated formula how the bonuses are constructed, but the underlying drives are ROIC and net revenue growth.

The structure is distinct because it requires mandatory reinvestment rather than granting stock options, thereby avoiding shareholder dilution. Senior executives must use a significant portion of their after-tax bonus—typically 75%—to purchase existing shares on the open market, which are then locked in escrow for three to five years,. This creates a “conveyor belt” of equity that ensures managers have a substantial net worth tied to the company’s long-term performance, aligning their interests with shareholders and turning employees into “partners” who share in the downside risk of capital allocation decisions.

Topicus.com Inc (TOI)

Now that we have briefly explained how CSI operates and what sets it apart, we can move on to Topicus.com. While Topicus is one of CSI’s operating groups, it was publicly listed for specific reasons that we will explain in this chapter. Understanding CSI is crucial to understanding Topicus. If you are a Topicus shareholder and haven’t read Mark Leonard’s letters (link), we highly recommend doing so!

Topicus.com: The Rise of CSI 2.0

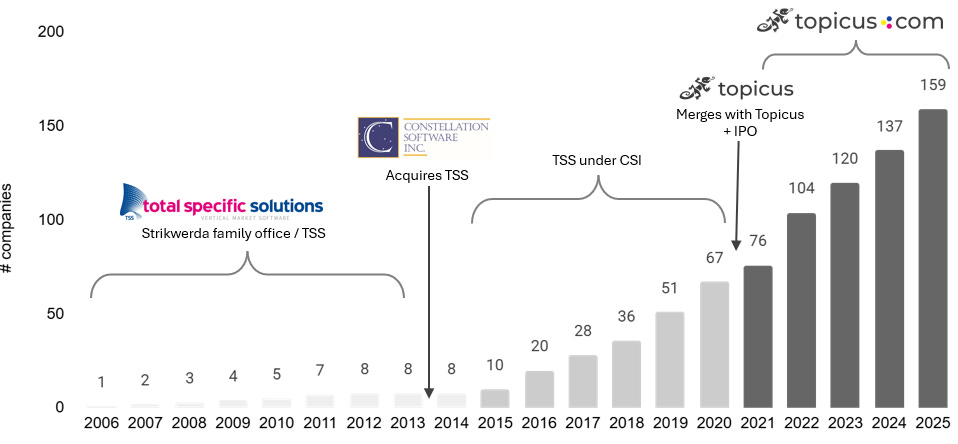

In December 2013, Constellation Software (CSI) acquired Total Specific Solutions (TSS). This was a pivotal moment for Constellation as it marked their largest acquisition to date. TSS generated annual revenue of €174m, and according to CSI, the purchase price was €240m (approximately 2.65x TSS’s 2013 forecasted net maintenance revenues).

At the time, TSS was the largest Vertical Market Software (VMS) business in the Netherlands, owning software companies dedicated to healthcare organizations, governments, and financial institutions. Founded in 2000 by Dutch entrepreneur Rinse Strikwerda, TSS operated as an independent investment company and remained a family business until the CSI acquisition.

The remainder of this research piece is exclusive to paid subscribers.

For a small monthly fee, you can unlock full access to our entire library of Deep Dives (including detailed financial models) and receive a new, comprehensive research report every month, along with regular updates. Since May ’25, we have covered:

Your support directly fuels this platform. Every dollar is reinvested into better resources and data, allowing us to produce even higher-quality research for you.

Following the acquisition, TSS was integrated into CSI, becoming one of its key operating groups. With access to CSI’s know-how and capital resources, TSS began to scale its acquisition volume significantly. Robin van Poelje, the CEO of TSS prior to the acquisition, remained at the helm to steer this growth. From 2015 onwards, the deal volume increased rapidly.

In 2020, a unique investment opportunity arose: a potential acquisition of Topicus. This was a substantial target with revenues of €100m—a stark contrast to TSS’s typical acquisition target size of around €5m.

Topicus was open to acquisition but insisted on retaining its own identity rather than being absorbed. To bridge this gap, Robin van Poelje proposed a unique solution: merge Topicus with CSI’s existing European group (TSS) and spin the combined entity out as a separate public company. The strategy worked. The entity was renamed Topicus.com Inc. and listed on the TSX Venture Exchange in February 2021. Mark Leonard explained the reasoning vividly in the acquisition press release:

“The plan to create a publicly listed operating group... was a key part of our discussions with the Topicus founders. They didn’t want their legacy disappearing into the craw of an omnivorous conglomerate. While they knew that Topicus would have autonomy within Constellation, they also wanted identity.”

While Topicus.com shares CSI’s DNA regarding capital allocation and decentralization, it possesses a distinct “mutation” in its operational strategy. Unlike Constellation, which typically buys companies and manages them as autonomous islands to maximize cash flow, Topicus focuses heavily on “connectedness.”

Source: Capital Compounding

Topicus actively encourages integration between its operating units to create comprehensive software suites. By ensuring their products can talk to one another, they build powerful ecosystems within specific verticals (such as education or healthcare). This allows them to cross-sell more effectively and develop new products internally, driving a higher rate of organic growth than is typically seen in the broader Constellation portfolio.

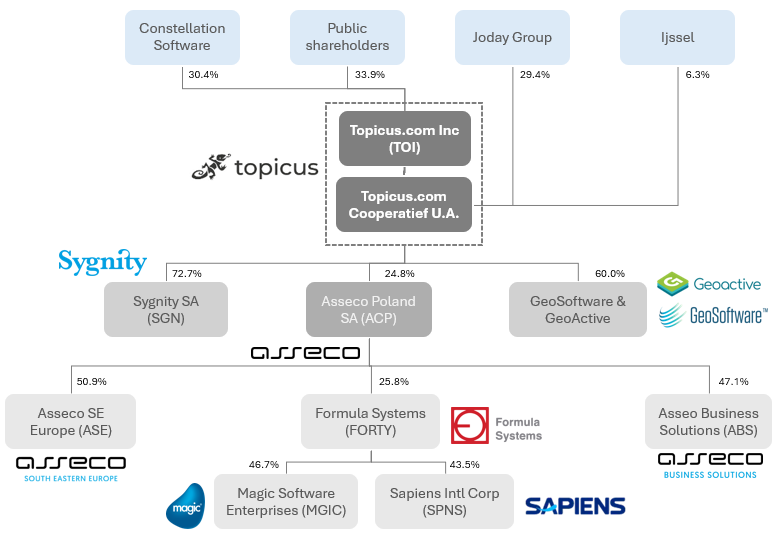

Today, the ownership structure reflects this unique history: Constellation Software owns roughly 30% of the shares (holding super-voting rights), the Strikwerda family owns approximately 30%, the original Topicus founders hold roughly 9%, and the remainder is held by public shareholders.

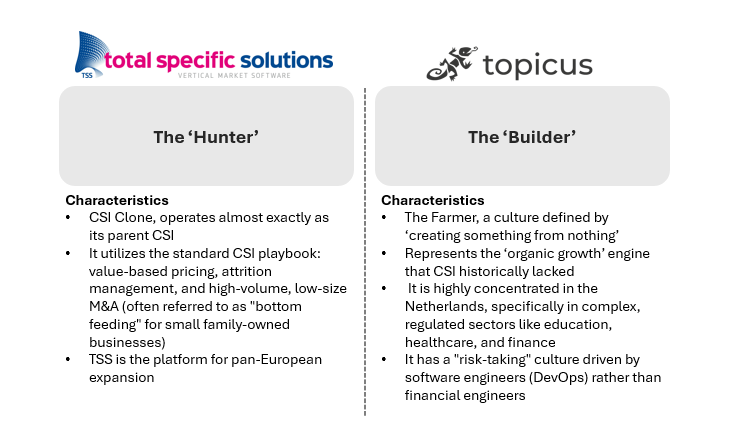

The ‘Hunter’ versus the ‘Builder’

When Topicus was acquired, a key stipulation from the founders was that Topicus must retain its unique identity. TSS and CSI agreed, rebranding the new entity as Topicus.com Inc. with Daan Dijkhuizen (former CEO of Topicus BV) appointed as CEO of the group. However, he served in this role for less than a year before stepping down to focus on running the Dutch operations instead.

Source: Capital Compounding

Insiders suggest that the political pressure of focusing on M&A and capital allocation—rather than operational building—was a mismatch for him:

“But he stepped down because he didn’t get the energy from working with Ramon Zanders and Robin. He didn’t feel strong enough to push the Topicus culture within TSS, because there are 1,200 employees and TSS has about 4,000, maybe a bit more…

…He mentioned that when he became the CEO of topicus.com, he lost some of his entrepreneurial spirit because he had to deal mainly with large investors interested in buying shares of topicus.com. I think the stakeholder management and the political aspects of being the CEO of a Toronto Stock Exchange-listed company didn’t excite him as much. Then they gave him this playground with the funds.” (Former executive, Topicus, ’24)

That “playground” is formally known as VMS Ventures. While the move may look like a sidelining, it was likely a strategic necessity: the Board realized that the “Builder” culture could not survive directly inside the “Hunter” (TSS) machine. By moving Dijkhuizen to VMS Ventures, they carved out a dedicated space to keep that organic growth spirit alive, separate from the strict capital allocation demands of the public entity.

Nevertheless, Daan’s voice has clearly become less dominant within the wider group. The CSI/TSS culture is now the primary driver, a shift visible in the ownership structure. Annual reports show that the former Topicus founders (via IJssel B.V.) have steadily decreased their position in Topicus.com (from ~9% in ’21 to 6% in June ’25). In stark contrast, key figures from the CSI/TSS side, like Robin van Poelje, have largely held or increased their stakes. This divergence signals more than just standard diversification; it highlights a fundamental transfer of power.

Historically, Topicus BV reinvested almost every euro of profit back into the business to fund growth and innovation, whereas CSI focuses on distributing cash or solely funding acquisitions. While the “Hunter” culture has won the leadership battle, I believe the lingering influence of the “Builder” DNA is why organic growth at Topicus remains stronger than at CSI. Ultimately, the value of the company may well depend on this ongoing friction: the discipline of the Hunters preventing waste, and the creativity of the Builders preventing stagnation.

Minority stake in Polish VMS serial acquirer Asseco

This year, Topicus entered a new stage of growth by acquiring a minority stake of ~25% in Asseco Poland S.A. (ticker: ASC.PW) for approximately €408m (using more than ’25 expected FCF).

At first glance, this transaction may seem odd. Topicus typically buys smaller private businesses or the occasional mid-sized one (like Cipal, with €110m gross revenues). However, if you revisit Mark Leonard’s shareholder letters from nearly 20 years ago, there is nothing strange about this deal. As he explained in 2008:

“I am often asked why Constellation takes minority interests in other public software companies. The answer is simple (value!), but it can be complicated by our investment horizon and by our requirement that the company have competent ownership…

… On ten occasions, however, we have also participated in the purchase of significant minority positions in public software businesses. Usually, these minority interests were purchased for less than their intrinsic value, and for far less per share than we would have had to pay for the entire business. While these purchases tend to be at the “value” end of our investment spectrum, they often carry incremental risk because we lack access to information concerning the long-term trade-offs that the businesses are making. Even excellent managers of public companies are initially uncomfortable allowing us to join their boards to get access to this information, suspecting us of dire motives or a short-term orientation. We have the same objective when we buy a piece of a business as when we buy 100%, i.e. we want to be a great perpetual owner of an inherently attractive asset. If we are allowed to join a public company’s board, we offer to sign an agreement that will limit our ability to make an unsolicited take-over bid. This allows existing long-term shareholders of our public investees to continue to enjoy the benefits of ownership. For shareholders with similar objectives to ours, we believe that we are an exceptional co-investor.” (Mark Leonard, CSI, 2008)

True to this playbook, Topicus signed an agreement capping their stake at 27.96% of Asseco’s share capital. In exchange, they secured three board seats for Robin van Poelje (CEO of Topicus.com), Ramon Zanders (CEO of TSS Europe), and Christopher Siemiaszko (Chief Data & Analytics Officer at CSI). The latter appointment is particularly interesting: Siemiaszko is fluent in Polish, and his presence signals that CSI is serious about bringing data-driven capital allocation to Asseco. Together, the group holds about 33% of the voting rights.

TSS also released an open letter to Asseco shareholders, in which snippets of the CSI playbook are clearly visible:

“Markets fluctuate. We aim to be an active shareholder focused on long-term value creation. We have no short-term share price targets. We observe that the current share price already suggests that the market is anticipating potential outcomes of our partnership. Looking ahead, we believe value will be created by focusing on margin expansion, growth in annual recurring revenue (ARR), and disciplined capital allocation. This underlines the importance of aligning management’s interests with those of shareholders.

Every złoty has alternatives: product investment, selective acquisitions that clear high hurdle rates, dividends, buybacks, or alignment programs. We will favor the option that we believe increases long-term per-share value.” (Ramon Zanders, CEO TSS Europe, Oct’25)

The Financial Logic: A Levered Yield Play

By my calculations, the deal structure alone—assuming absolutely no operational improvements—already meets Topicus’s minimum 20% hurdle rate. Let’s walk through the math.

Topicus paid 85 PLN per share for roughly 20.6 million shares. At this price, Asseco’s implied market cap is ~7.06 billion PLN. Based on LTM 2025 Free Cash Flow (FCF) of ~946.5m PLN, the entry valuation represents a P/FCF of 7.5x, or an FCF yield of 13.3%.

To fund the deal, Topicus utilized a €200m Schuldschein (private debt) with an estimated interest rate of 4.25%, resulting in an annual interest expense of ~€8.5m.

Here is how the leverage boosts the return:

Look-Through FCF: The FCF attributable to the Topicus stake (13.3% yield on €408m asset) is ~€54.4m.

Net FCF to Equity: Subtracting the interest expense (€8.5m) leaves €45.9m.

Equity Investment: Topicus put in €208m of its own cash (Total €408m - €200m Debt).

The Result: €45.9m / €208m = ~22% Levered IRR

It is crucial, however, to distinguish between the cash Topicus physically receives and the value created. The dividend yield provides a cash-on-cash return of ~5% (which covers the debt service). The remaining ~17% is retained within Asseco. This retained capital is where the “active partner” strategy becomes vital—Topicus must ensure this capital is deployed effectively.

Although Topicus holds a minority stake and lacks full control, the presence of three senior executives on the Board suggests we can expect meaningful improvements. My hope is that the following three shifts will play out:

Margin Expansion: Asseco’s EBITDA margins could improve from ~15% today toward ~25%. This will likely happen via benchmarking, using the standard CSI metrics (e.g., maintenance retention rates, R&D efficiency) to identify gaps. Note that Asseco is a “Federation” of subsidiaries (like Formula Systems), so this benchmarking will need to penetrate multiple layers of management, which is more complex than fixing a single P&L.

Strategic Capital Allocation: Currently, Asseco pays out 40-50% of earnings as dividends. While Topicus typically prefers deploying all cash into M&A, they may tolerate the dividend in the medium term to maintain alignment with the founder, Adam Góral, who relies on this income. However, over time, I expect Topicus to steer the remaining 50% of cash flow (and any margin improvements) much more aggressively into acquisitions, leveraging CSI’s database of 70,000+ leads.

Strategic Extension: Asseco is the perfect vehicle for Topicus to conquer Eastern Europe. Just as TSS was the engine for CSI in the Netherlands, Asseco can be the engine for Topicus in the CEE region.

The next 12–18 months will determine if these expectations materialize. However, one thing is certain: CSI and Topicus do not deploy capital unless they see a path to their 20% hurdle rate. Given the attractive entry valuation and the smart use of leverage, if they successfully implement the points above, I expect a very strong IRR.

With the minority stake in Asseco, you can see how the decentralized structure is continuing.

Source: Capital Compounding, company reports

Sygnity Case Study: The Proof of Concept

In 2022, Topicus acquired a majority stake (~72%) in Sygnity, a smaller, listed Polish IT integrator, for 12 PLN per share. Sygnity produces mission-critical software for the government, energy, and banking sectors—essentially a “mini-Asseco.”

In the last three years, Sygnity’s metrics have improved dramatically [reference to graph]. Management reset prices (especially in government/utilities) to match the value proposition, stopped bidding on low-margin “prestige” projects, and focused entirely on profitable recurring revenue.

Once the core was fixed—which took about 18 months—they began using Sygnity’s cash flow to buy smaller software firms, turning the company into a compounder itself. To put this in perspective: Sygnity did zero acquisitions between 2016–2022 and was forced to sell assets to survive. Post-Topicus, they have closed 3 deals in ~2 years.

Source: Capital Compounding, company reports

It is important to note the difference: Sygnity was a distressed asset priced for bankruptcy (yielding an 8x return), whereas Asseco is a stable asset priced for mediocrity. We should not expect Asseco to replicate Sygnity’s 800% (zl 12 to gain. However, the playbook remains the same. If Topicus can achieve even a fraction of the same operational success with Asseco—moving it from “Good” to “Great”—shareholders can expect significant value creation.

The Moat of Topicus

“The barrier to starting a conglomerate of vertical market software businesses is pretty much a cheque book and a telephone.” (Mark Leonard, CSI, 2013)

Mark Leonard’s famous remark suggests that the barriers to entry in this industry are low. In theory, he is right: anyone with capital can copy the CSI model, and indeed, many private equity firms and copycat acquirers are trying to do just that. However, the barrier to success is significantly higher. The true moat protecting Topicus and CSI is not merely financial—it is organizational, data-driven, and cultural.

The Proprietary Data Engine

Insider sources estimate that CSI’s proprietary database contains approximately 70,000 leads. While the exact number is guarded, the strategic value of this asset is undeniable.

This database is not just a list; it is a “CRM of relationships” built over decades of manual updates and founder nurturing. It allows Topicus to track potential targets years before they are ready to sell.

The Advantage: Competitors without this data must rely on business brokers to find deals.

The Flaw: Brokers engineer auctions, which maximize competition and drive up prices. By sourcing deals directly from their proprietary database, Topicus avoids these auctions, often paying fair value rather than an inflated premium.

The Benchmarking Machine

With over 1,100 acquisitions completed across the group, CSI and Topicus possess a dataset that no competitor can match. Every acquired company’s income statement is mapped to a standardized template, allowing for instant benchmarking.

This data gives them the conviction to pull operational levers that others would fear. As a former M&A executive explained in 2024:

“CSI have confidence to do [price increases] because by owning 900 businesses, they know exactly what will happen. If you own 20 businesses, you would be nervous about the impact... They also look at price equalization... and use ‘Utopia Grids’ which have customers on the side and modules across the top. They look at who has what, and all the blank modules are back-to-base opportunities. These are all simple, but you can move the needle by overlaying even half of them.”

This “Utopia Grid” methodology allows Topicus to systematically uncover revenue synergies (cross-selling) that a typical financial buyer would miss.

Structural Decentralization

The most defining characteristic of the Topicus moat is its decentralized capital allocation.

Unlike traditional conglomerates that slow down as they grow (”bureaucratic sclerosis”), Topicus operates as a federation of hundreds of small, agile business units. This structure allows them to scale acquisition volume indefinitely. They do not rely on a single central investment committee to approve every €5m deal; instead, they empower local managers to deploy capital. This allows them to process hundreds of small transactions annually—a volume that would choke a centralized private equity firm.

The “Perpetual Owner” Advantage

Finally, Topicus’s status as a “Permanent Home” creates a powerful psychological moat.

Private Equity firms typically operate on a 3–7 year timeline, looking to “flip” businesses for a quick exit. This often involves aggressive cost-cutting and bundling. In contrast, Topicus promises to hold the asset forever.

The Founder’s Dilemma: For owner-operators, their business is their life’s work. They care deeply about their legacy and the job security of their loyal staff—”the lady who delivers the coffee.”

The Trust Discount: Because Topicus guarantees autonomy and stability, founders often choose them over higher bidders. This trust allows Topicus to bridge valuation gaps, securing assets at attractive multiples because they offer something money cannot buy: legacy preservation.

Summary

The moat is self-reinforcing. The “Never Sell” philosophy builds trust, which leads to proprietary deal flow. The Data Engine ensures those deals are priced correctly. The Decentralized Structure ensures the acquired companies are managed efficiently without bureaucracy. This combination creates a high-retention culture that competitors, armed only with a cheque book and a telephone, struggle to replicate.

Will AI disrupt Constellation and Topicus?

Artificial Intelligence is poised to reshape industries, though the velocity and magnitude of this disruption remain subjects of intense debate. Currently, the market consensus suggests that horizontal software (broad, industry-agnostic tools like Salesforce or HubSpot) faces the most immediate threat of commoditization. However, Constellation Software (CSI) and Topicus have not been immune to this sentiment; their share prices have reflected investor anxiety, compounded by the fact that they have traded at historically high multiples in recent years. A valuation re-rating, therefore, may be a healthy correction rather than a signal of fundamental decay.

The prevailing bear case is straightforward: AI will commoditize code. If software becomes cheaper to write and easier to replicate, switching costs—the primary moat of Vertical Market Software (VMS)—could erode. In this narrative, attrition rises as customers flock to AI-native competitors that offer “good enough” solutions at a fraction of the cost.

While code may become a commodity, proprietary data and workflow integration remain scarce. The “VMS defense” relies on the fact that legacy systems hold the “system of record” data (e.g., historical tax records, patient health history, or municipal utility usage) that AI models need to function effectively.

Proprietary Intelligence: As long as Topicus and CSI companies maintain ownership of the underlying data, they possess the raw material required to build the best AI models for their specific niches. They can pivot from selling “software” to selling “intelligence,” effectively turning a threat into a higher-margin product.

The Efficiency Lever: For a serial acquirer, AI is a double-edged sword that cuts in their favor operationally. If AI tools can automate coding, testing, and customer support, the cost to maintain these mature businesses could drop significantly. This would structurally increase EBITDA margins, allowing Topicus to extract even more free cash flow from its existing portfolio.

Ultimately, while the future is uncertain, the “death of software” narrative likely underestimates the stickiness of mission-critical systems. It is far more probable that incumbents will adopt AI to reinforce their moats rather than be displaced by it.

Most importantly, we do not yet see evidence of this disruption in the financials. The key metric to track is Organic Maintenance Revenue Growth. If this metric begins to trend negative, it would be the clearest signal that the “moat” has been breached—indicating that customers are actively churning to AI-native providers faster than Topicus can raise prices. Until then, the thesis holds.

Ideally, you would look at retention as that would be an early warning signal, but this data is not available to investors, so we have to with the organic revenue metric.

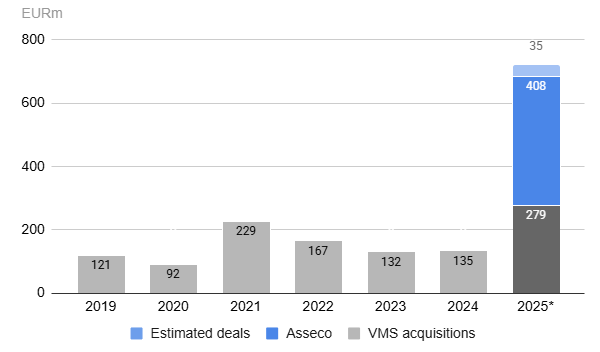

Financials and valuation

This year, Topicus has shifted into a higher gear of capital allocation. Including our estimates for Q4 ’25, the company has deployed approximately €725m—a figure that is more than double the Free Cash Flow generated by the business over the same period.

Source: Capital Compounding, company reports

We view this aggressive deployment as a positive signal. Based on the company’s track record, we are confident that this capital is being reinvested at high rates of return. Our specific analysis of the recent Asseco transaction points to a levered IRR of ~22%—a base-case return that excludes the significant operational upside available if Topicus successfully implements the CSI playbook at Asseco. Link to the model is at the end of this deep dive.

Valuation

Valuing Topicus.com is more complex than valuing a standard public company because of its unique ownership structure. However, the logic is straightforward once you separate the “accounting view” from the “economic reality.”

Earlier in this deep dive, we outlined the ownership structure of Topicus. Approximately ~35% of the underlying operating equity is held by the founders of TSS (29.4%) and Topicus (6.3%). In standard financial reporting, the cash flow belonging to these groups is deducted from the headline number, leaving us with Free Cash Flow Available to Shareholders (FCFA2S). On an LTM basis, this reported number is €204m.

However, if we include the FCF available for the non-controlling shareholders (the Joday/IJssel group), the Consolidated FCF (Diluted) rises to €330m. We believe this “Consolidated” view is the correct way to value the business. Even though that ~35% of cash technically “belongs” to the minority partners, Topicus does not pay it out as dividends. Instead, the management team retains that capital to fund new acquisitions. By looking only at the “Attributable FCF,” investors ignore a significant portion of the actual firepower the management team has at its disposal to compound value.

In most companies, “Non-Controlling Interest” refers to a passive partner who might demand a dividend or block decisions. At Topicus, the NCI consists of Constellation Software (Joday) and the Original Founders. These are not passive rent-seekers; they are active capital allocators who want to compound, not cash out. By adding back the NCI and using the diluted share count, we align our valuation with the actual economic engine of the business.

Finally, we must account for the Asseco Poland transaction. We can value this stake in two ways. The conservative (and in our view, incorrect) method is to count only the cash dividends received—roughly ~€10m per annum after interest. The superior method is the “Look-Through” approach, where we credit Topicus with its ~25% share of Asseco’s total free cash flow.

Asseco is a complex holding that consolidates many subsidiaries where it does not hold 100% ownership. Fortunately, in their latest presentation (3Q ’25), Asseco reported its own LTM FCF adjusted for its non-controlling shareholders: PLN 946.5m. Topicus’s ~25% share of this equates to roughly €54.4m. After deducting the estimated interest on the €200m Schuldschein (~€8.5m), the net look-through contribution is ~€45.9m.

This brings the total Consolidated Economic FCF to approximately €375m (CA$ 607m). Against a fully diluted market cap, this equates to a P/FCF multiple of ~26x.

Below, we lined out once more the steps we took to calculate the P/FCF multiple:

Source: Capital Compounding

Current situation and the opportunity

What makes the current setup attractive is the disconnect between narrative and reality. The “AI disruption” narrative has not yet played out in the fundamentals—it remains a story with a wide range of possible outcomes. Yet, the market is pricing Topicus and Constellation Software (CSI) as if they are already confirmed “AI losers.” This creates an asymmetric opportunity: if the market is wrong (or even just partially wrong), the returns from current levels could be substantial.

The Capital Deployment Machine

While the market worries about the future of VMS, the Topicus engine is firing on all cylinders. This year alone, the company has deployed approximately ~€725m (utilizing both FCF and debt capacity)—a record number. The contrast is stark: just last year, capital deployment was so slow that Topicus returned cash to shareholders via a special dividend. Today, they are deploying capital faster than they can generate it. This surge in activity suggests that management sees immense value in the market, precisely when investors are most fearful.

Ultimately, the only measure that matters for long-term performance was laid out two decades ago by Mark Leonard: ROIC + Organic Growth.

We trust Topicus management to maintain discipline; when they deploy FCF, we assume the ROIC is at least above 20%. Our deep dive into the recent Asseco deal—Topicus’s largest ever—confirms this discipline. Even without factoring in post-acquisition operational improvements, the Levered Free Cash Flow Yield on that transaction alone clears the 20% hurdle.

The Recession “Call Option”

A scenario we are seriously considering is the possibility of a recession. While a downturn combined with AI fears could depress Topicus’s own trading multiple, it would ironically be a boon for the business model.

Resilience: Mission-critical software tends to be the last thing customers cut, making Topicus’s cash flows durable.

Opportunity: As a perpetual buyer, Topicus benefits when private market valuations drop. If AI fears and a recession drive private multiples down, Topicus can deploy capital at even higher rates of return. Mark Leonard famously admitted after the 2008 financial crisis that his only regret was not buying more when prices were low:

“Constellation’s intangible assets has appreciated even during the recent recession... It seems intuitively appealing that as we go through an economic cycle there will be good times to organically grow maintenance revenues and good times to buy maintenance revenues, and that those events will rarely coincide. I only wish we had acquired more maintenance during the recession before acquisition prices rebounded.” (Mark Leonard, CSI, 2010)

Conclusion + Model

In the attached model, you will find a detailed breakdown of the financials, but the investment thesis is simple. Topicus has aggressively ramped up capital deployment—effectively spending next year’s cash flow today to lock in value. If they can maintain positive organic growth while continuing this pace of deployment, we expect an internal compounding rate (ROIC) of >20%. With the stock currently trading at ~26x P/FCF, this creates a highly attractive entry point for a long-term compounder.

Model: Topicus.com Inc (TOI)

Why we prefer Topicus over CSI

While both companies share the same DNA and are operationally interlinked, Constellation Software (CSI) faces a mathematical gravity that Topicus does not: the Law of Large Numbers.

CSI has reached a scale where capital deployment becomes increasingly difficult. To move the needle on a revenue base of ~$10B+, CSI must deploy massive amounts of capital annually. This forces them to increasingly compete in the “large deal” segment—an area saturated by Private Equity firms willing to accept lower hurdle rates.

Topicus, by contrast, operates with a significantly smaller base (~€1B revenue), granting it a much longer runway for high-growth compounding. It can still double its size primarily by acquiring small, sub-€10M VMS businesses. This is the “sweet spot” where competition is low, prices are rational, and proprietary relationships matter most. While the recent Asseco transaction demonstrates that Topicus is not immune to the need for larger capital deployment, we view this as an “opportunistic layer” on top of a healthy core engine, rather than a sign of saturation.

Furthermore, Topicus operates exclusively in Europe, a market that is structurally more fragmented than North America. Language barriers, distinct legal systems, and cultural nuances create natural “moats” that deter large US-based PE firms. In this environment, Topicus’s decentralized, relationship-driven approach is a potent competitive advantage.

With both serial acquirers trading at roughly the same P/FCF multiple, we prefer Topicus.

Disclaimer

The information in this article is provided for informational and educational purposes only. The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence. None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions. The author may or may not have shares of the company.

Great post. Thanks!

Thanks a lot for sharing. Probably the best analysis written about Topicus by a wide margin.