Auto Partner SA (ticker: APR.PW)

Polish aftermarket car parts distributor compounding at attractive rates

Our next deep dive will be about Auto Partner SA (ticker: APR.PW), a Polish aftermarket auto parts distributor with a leading position in Poland and growing rapidly in the EU. We visited the company and its management early June ‘25 and came back with a lot of new insights. The deep dive is set up as you are used to from us (intro, business model, market/competition, moat, management assessment, conclusion). In the financial sector, we also added a Google sheets model if you want to play around with the numbers yourself. Hope you enjoy this one!

Auto Partner SA

Auto Partner was founded in ‘93 and went public in ‘16 on the Warsaw Stock Exchange (WSE) under the ticker APR. Auto Partner is the #2 distributor in aftermarket auto parts in Poland. Since being listed, their growth has been impressive and revenues went up with a +25% CAGR. What is even more impressive is that Auto Partner built a decent export model from the ground up. It accounts now for more than 50% of total revenues. In ‘24, Auto Partner reached about ~zl 4.1bn in revenues (which is ~$1.1bn) and has a market cap of about $700m. AP employs about 2,800 FTEs.

Small disclaimer, as a shareholder, I am biased, so take everything with a pinch of salt what I write. Nevertheless I try to be as objective as possible.

Investment thesis

Distributors are generally speaking good businesses to invest in. Most distributors grow via M&A, especially in replacement parts. Auto Partner stands out from that point of view as it grows organically, but there a couple of other reasons why this is an interesting business:

Auto Partner has an impressive track record. In the last 10 years, revenues and net profit grew with CAGR’s of respectively +25% and +30%. Even though it is one of the smaller players in Europe, the margins are comparable if not even better than its larger competitors.

Auto Partner ticks the boxes as an investable business, high ROIC which is almost fully reinvested in further growth, founder-led business where the owner has a decent skin in the company.

Auto Partner has a solid market share in Poland as the #2 player in the country. In ‘26 it will open a new distribution center close to the border of Germany which should fuel further growth in Western Europe.

Trading at a cheap valuation of 13x forward P/E for a business that could continue to grow about 10-20% over the next five years.

Introduction

The founder, Aleksander Gorecki still owns about 44% (directly or indirectly) of the outstanding shares and started the business in its very early days from his 90m2 apartment, where he showcased parts in the hallways and personally delivered them to customers. Over the years they have been expanding by constructing large warehouses, offering a wider range of products and a well developed logistics infrastructure.

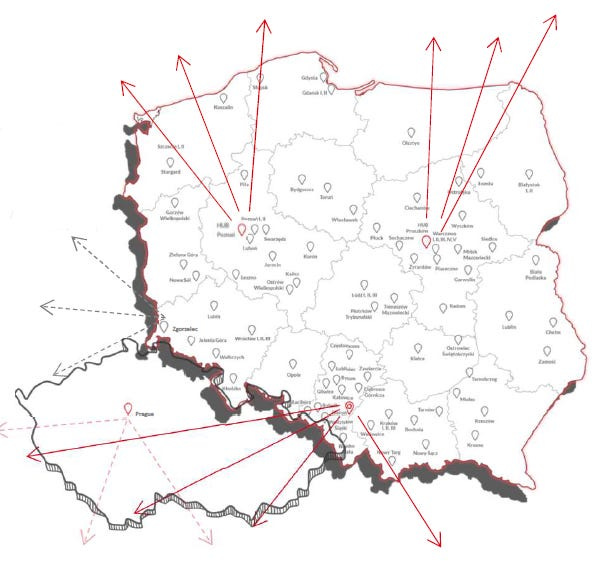

Nowadays, the headquarter and main distribution center is in Beirun, which is south of Poland. The DC has an area of 52,000m, but in total AP has about 160,000m2 warehouse space. Other (smaller) warehouses are: Pruszkow (12,500m2), Poznan (13,500m2, and Myslowice (24,000m2). Auto Partner also has 118 branches in Poland with warehouse space. To conclude, AP also has two warehouses in Prague. Below you see the locations of the DC, warehouses and branches in Poland.

Around 50% of its parts are sold in Poland via branches to repair shops (63%), specialized stores (27%) and non-specialised repairers and retailers (10%). The other 50% is exported to neighboring countries and via sales representatives sold to stores, wholesalers and distributors. Its product portfolio includes spare parts for car systems, parts and accessories for motorcycles, filters, oils, car chemicals and accessories. In the last couple of years, they have also been involved in e-commerce where small items are shipped via mail directly to the customer.

US versus European market.

I think most of the investors who are reading this piece are familiar with distributors such as AutoZone and O’Reilly Auto Parts and their dominance in the US. AutoZone and O'Reilly together have a market share of about 70-75% in the US. Auto parts in the US are more homogeneous (more of the same cars are driving in the US) and hence both sell a large part of private label products.

I assumed there was a similar playbook in Europe. But nothing was further from the truth. The two largest distributors in Europe have together about ~10% market share.

The European market is fragmented, you deal with cultural differences and products are far less homogeneous as there are many different brands of cars and models in Europe. Also there are more layers in the value chain which can differ per country. Hence, in Europe there are far more local distributors.

LKQ, is the market leader in Europe and operates via a ‘roll up’ strategy by acquiring smaller to mid-sized distributions in Europe. Sounds like a good business model, but I haven’t been impressed by what I have seen so far from them. Revenues barely grew in the last 5 years (see graph). Net leverage is elevated at 3.3x, it has a high dividend pay-out ratio of ~45%. And with a FCF margin of 4-5%, it spends about 2-2.5% of remaining FCF on growth.

It doesn’t look like a winning strategy at all. M&A doesn’t always work well. LKQ sold for example in ‘24 their Polish business (which they acquired a couple of years before!) to MEKO, a market leader in spare parts in the Nordics. Justin Jude, Executive Vice President and Chief Operating Officer of LKQ, stated:

“The evaluation and streamlining of our asset base is a core strategic pillar for our Company. As part of this ongoing process, and after thorough consideration, we have made the strategic decision to divest Elit Polska. We believe the business is complementary to MEKO and will perform strongly under their leadership.”1

Auto Partner has been grown organically and the last acquisition dates from ‘08 where they expanded in the Czech Republic. Management highlighted to me that this wasn’t a success and since then focused solely on organic growth. My impression when I went to visit the company is that management is competitive and hungry to grow further, but remain humble and realistic. They are not settling for less, but also don’t project far in the future. With a horizon of let’s say 2-3yrs they are working with and in the meantime, they try to improve the business incrementally. There is no bureaucracy at the company.

Poland is in general an interesting country for investment purposes. A sales account manager who is covering the Benelux at Auto Partner I spoke to, called Poland the ‘China of Europe’. Both countries have transitioned from communism to capitalism. Both countries are growing fast and competition is extremely fierce. Poland is an outlier in Europe with its growth. Being part of the EU gave Polish companies a venue to expand further. Auto Partner is one of these companies.

Business model

The business model of a distributor is fairly straight forward. A distributor sits between the customers and the suppliers. It doesn’t produce and capex is limited to opening branches and distribution centers. Most of the capital deployed is in inventory. The quicker you turn over your inventory, the more cash the business generates. Opex is mainly in overhead, transportation and warehousing.

AP works with 350 suppliers including their own private label MaXgear and hence has access to over 250,000 products from these suppliers. Buying happens in an alliance with GlobalOne to make sure there is enough bargaining power. Inventory is managed mainly via their distribution center in Beirun and otherwise via their warehouses. In Poland the branches can also hold a small amount of inventory. About ~70% of the customer orders are placed online. This is not unique and I have seen this with major players like LKQ here in the UK. From the DC / warehouses, the branches get replenished frequently. Customers can pick up products when available from the branch or delivered by Auto Partner. Below you will find a picture of a recently opened branch in Beirun.

AP delivers products 2-8 times a day from their branches. AP also created MaXserwis, where it partners with mechanics whose purpose is to help them stay up to date on car repair knowledge, it also leases specialized tools (Autozone does the same in the US) if needed. These mechanic shops tend to be more loyal to AP and hence do more business. Car mechanic shops also have the opportunity to be listed on the website, an aggregator for car owners to search for mechanics shops in their area.

Export model

Outside Poland, AP does not have branches and hence the customers are mainly local distributors, wholesalers and stores who then sell to the end customer. Auto Partner sells to these distributors which are linked to AP’s IT systems. So basically Auto Partner is using these local distributors as ‘branches’ and this has been extremely successful considering revenues from exports are now higher than revenues in Poland. Inter Cars, the bigger distributor in Poland missed out on this opportunity.

There is no doubt that Auto Partner (and Inter Cars) receive lower prices compared to its competitors in Western Europe from suppliers due to its location and currency. And I spent a lot of time on this part to figure out if this can break the thesis up at some point. The prices between countries will never be that big. According to a former export director at Inter Cars:

Because according to European Union law, Bosch cannot forbid them this kind of activity. Because each company, if they bought something in one country, they can sell in another country. This is the European Union. That means the switch rate, something like that. Of course, Bosch is doing some discussing every year with each company. By doing that, they do some price harmonization between the countries if the gap is not so big, I don't know. The gap between the prices will be 5%, 10% nobody will bother. If the gap between the prices is 25%, 30%, then somebody will take over.

Bosch, for instance, they are doing very often the different part numbers for each country to protect this market. So even if we are talking about the same wiper blade, in France, there is a different code number with different EM code. And in Poland, is different part number with different EM code.

But Auto Partner managed to grow their export business much faster than Inter Cars. It can not only be about price. Convenience is also a factor and that is where Auto Partner worked on very well in the beginning. Lower prices and easy access to the products resulted in rapid growth. Again according to same export director:

It not depends only on the prices then. It's always something what you offer for these customers additionally. And the West Europe is mainly focusing on the easiest solution. And unfortunately, Inter Cars, due to this big amount of the goods in the offer, they couldn't, for instance, supply the FTP connection with the stock level or with the prices. That’s because if you are discussing with some distributor in Belgium, usually, this is some distributor or some companies who will cooperate with other distributors, with the distributor in the country.

If you are discussing with some small dealer in Belgium, he is, I think, connected with Zak, LKQ group or Sator. So they are buying every day from Zak or from Sator. And if you want to offer them something better, then first, they will ask you, okay, give me FTP connection, I will connect this to my software and I will see everything. I will compare everything very easily. And on these two fields, Auto Partner is better. Because Auto Partner is working on the Microsoft Dynamics AX. This is much more common for the Word, Microsoft, okay, open the door. So there, it's much more easier to prepare for customer, the connection.

Inter Cars, unfortunately, is running on the day one of their own system, very old one, not user friendly and for the equipment, I was fighting with our IT department, prepare the easy API for our customers with easy instruction what they need to do to connect and to see the availability and price because they want to see only that, two things, availability and price.(August ‘22)

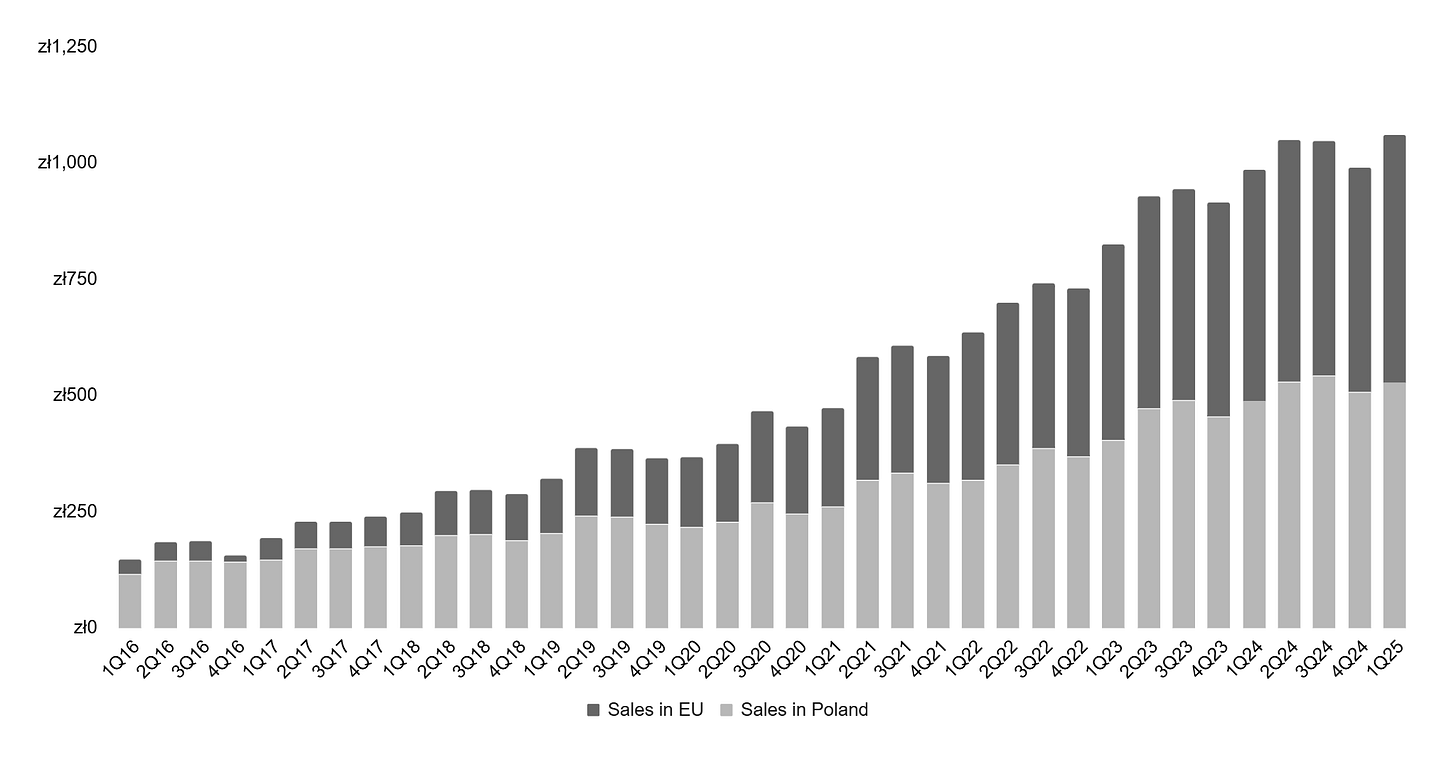

It seems to me that Inter Cars was not focused that much on it than Auto Partner. Below I plotted the quarterly revenues in the EU since being listed.

You would think this might be a flawed business model, at least that is what I initially thought. In the end, AP doesn’t control how the service / speed of delivery etc is towards the end customer. Let’s assume the majority of these customers are mechanic shops who need their products as soon as possible. But on the flip side, AP is able to scale the business by just having a good relationship with these local distributors, taking no inventory risk, no capex of setting up the branches and overhead costs. And the fact that the industry is still so fragmented, i.e. local relationships between mechanic shops and distributor/stores are so sticky, it is very hard to break into. It took me a while to realize this.

These distributors manage their own inventory and hence can easily wait a day to get their products delivered to them. And what if the distributor or store is not upholding the quality of service to its own customers? Then eventually AP will do less business with them, but no harm done, there will be another distributor who pops up to do business with.

In Germany alone it estimated that there are about 2,000 to 4,000 independent auto parts stores and distributors!

To conclude, We consider the way AP is using these local distributors as ‘franchisees’ and understand that even mechanic shops indirectly via these local distributors have access to the digital catalogus of AP. See below a visualization how this works

New DC

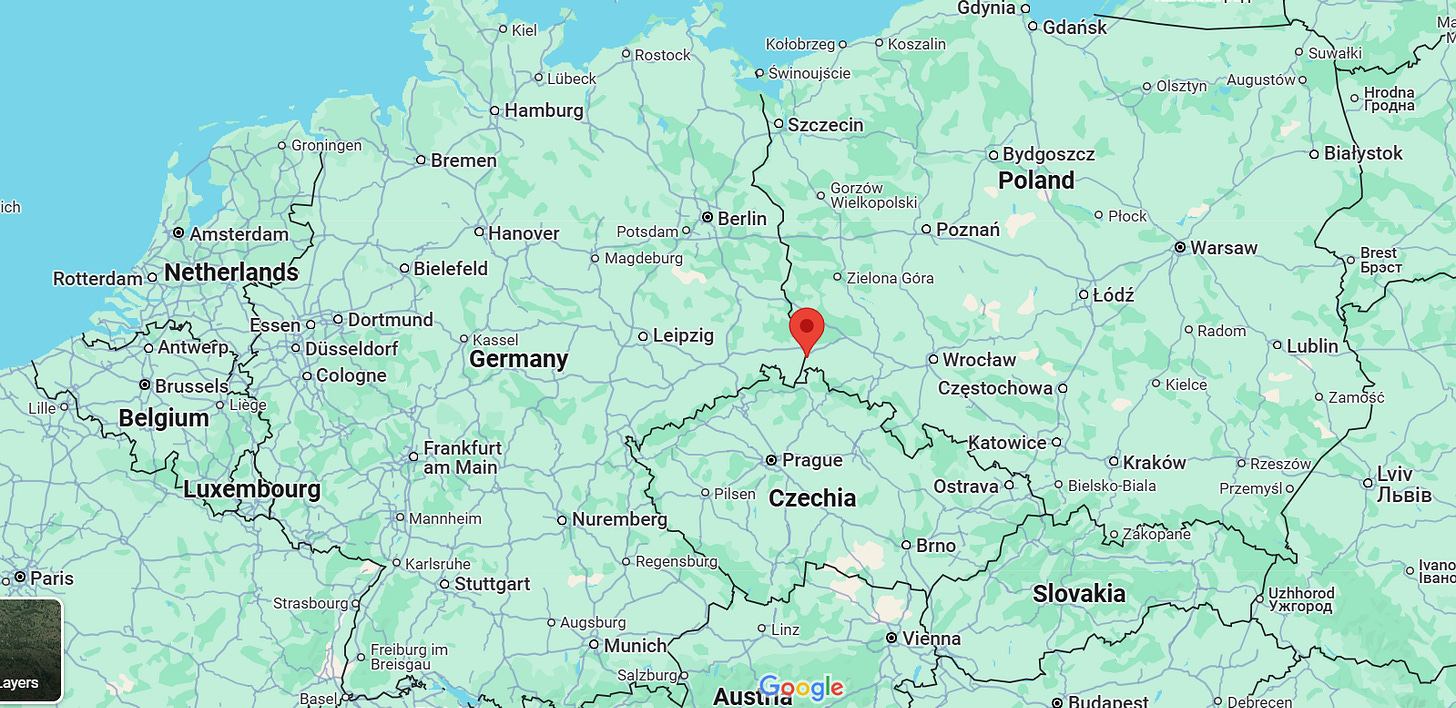

Auto Partner will open a new distribution center early in ‘26 with a warehouse space of 30,000m2, expanding total warehouse space by almost ~20%. But more importantly, if you look at the location on the map, it is right next to the border of Germany. Some inventory from the main DC will move there and new inventory will be placed.

You can imagine with the new DC, AP can reach more customers in W-Europe, it can ship faster, cheaper (4hrs from Beirun DC) which should increase the turnover of inventory and thus revenues even further. It is a development we will be monitoring very closely

Main competitor Inter Cars, mainly work with branches in Eastern Europe. They had some in Western Europe as well, but they closed down the branches and copied AP’s business model. In ‘19 Inter Cars stated this in their annual report regarding branches in Italy:

The management of the Inter Cards Group decided to restructure the Italian company Inter Cars Italia s.r.l., which has not been profitable. Following a profitability analysis of particular areas of its activity a decision was made to change its business model by closing all 6 branches and continuing direct sales to shops and warehouses offering spare parts. This way the company should arrive at the desired operating margin. The future restructuring costs, including severance pays for employees required by the applicable law, the costs of termination of contracts of lease of office and warehouse space, as well as other administrative costs will be paid from a reserve of PLN 8,600k recorded in the first half of 2019.

It remains to be seen how well Inter Cars will do going forward on their export model. The market is big enough for both AP and Inter Cars to grow.

Market and competition

Before we dive into the competition, We think it is important to understand and analyze the underlying auto market in Europe because in the long run, this will drive potential demand for auto parts.

Two indicators are important to monitor demand for auto parts: 1) growing use of vehicles and 2) the average age of a passenger car in the EU. According to various sources the use of vehicles in the EU has been steadily growing since ‘10 from ~240m to about ~290m in ‘24. The average age of a passenger car in the EU is estimated to be around 11-12 years (from 9 years in ‘10).

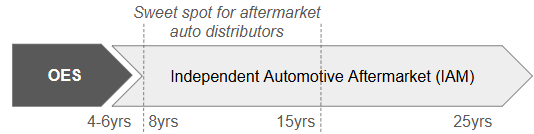

Relatively new cars (up to 4 years) are under warranty and hence will not go to an independent mechanic shop for repairs (the main end customer for AP). According to competitor Inter Cars, the sweet spot for aftermarket auto parts distributors is between 8 and 15 years.

Total Addressable Market

The TAM for independent aftermarket auto parts is difficult to estimate, as I have read reports being between €100bn to €200bn so assuming the worst case scenario, TAM of about €100bn.

The market is fragmented with the largest player, LKQ Corporation, having about 6% market share in Europe. Second largest player is Polish distributor Inter Cars with a market share of about 3.5%. Third largest player is Genuine Parts Company (GPC), which in Europe operates under the name Alliance Automotive Group and has less than 3.5% market share. The rest of the larger players have about 1 to 2% market share. GPC and LKQ grow revenues in Europe mostly by doing M&A, organically both players don’t really grow. This is what GPC says about the auto parts market:

“Our Automotive segment operates in a large and fragmented market with a total addressable market greater than $200 billion. The majority of the automotive aftermarket is comprised of small, local competitors which creates an opportunity to actively pursue strategic acquisitions and bolt-on store groups where we can bring scale, advanced technology, and supply chain efficiency to differentiate ourselves from competitors.” (source: annual report ‘23 GPC)

The independent auto parts aftermarket in the EU is expected to experience moderate growth over the next five years with a CAGR of 2-3% according to various sources, driven by factors such as vehicle aging, increasing vehicle parc, and consumer demand for cost-effective repairs.

Poland

If we zoom in on Poland, which by itself is one of the largest European aftermarket car parts as well, Inter Cars has about ~30% market share and operates in Poland 248 branches at the moment. Auto Partner has 118 branches. Inter Cars hasn't increased their number of branches in Poland for the last 5yrs, while AP went from 80 to 116 branches (+45%).

The other players are Inter Team (acquired by LKQ in ‘18) and has been losing market share the last couple of years. Last year it was sold to MEKO. H.M Gorden is another player with ~7% market share, but eventually filed for bankruptcy early in ‘25.

Competition is fierce in Poland, but according to management the belief is that over time Inter Cars and Auto Partner will be the leading players that remain. Outside Poland, it is Auto Partner focusing on W-Europe with their export model and Inter Cars on CEE with its 660 branches.

Inter Cars is Auto Partner’s largest competitor. It is a larger scaled version of Auto Partner. But there are some differences between both companies. Inter Cars relies heavily on their branch network. They copied Auto Partner’s export model, but weren't really committed to it. From various sources I hear that Inter Cars runs a less cost disciplined model than Auto Partner. You see this reflected in the margins when you compare them.

Moat

The business has been run extremely efficiently, and I believe that Auto Partner’s moat, although narrow, lies within their cost leadership. This is embedded in the culture and I felt that when I visited the company. Conversations with management and other investors confirm this.

We are dealing with a small cap here, although the business has existed for more than 30 years, there is still a long runway for AP. By opening more DC’s in focusing on Western Europe, Auto Partner is able to widen its moat.

As you saw in the competition part, there are dominant players in Europe. It is not like the US where 2 players dominate the market. This might be the case in Poland, but it is not in Europe. The market is too fragmented. The playing field is more level.

To put things into numbers, see below the margins of all major players in Europe incl Auto Partner.

Even though Auto Partner runs on a much smaller scale than Inter Cars, it manages to produce for the last 10 years a better margin than Inter Cars.

Management / culture

Aleksander Gorecki is the founder and CEO of Auto Partner with currently ~44% ownership. The most senior persons below him are Andrzej Manowski and Piotr Janta. My impression is that Aleksander is operating nowadays more in the background while Andrzej and Piotr running the business operationally.

Andrzej Manowski has been involved with Auto Partner for 20yrs and since ‘07 VP of the Management Board. He is responsible for the geographical expansion, including the development of the export activities, he also supervises IT projects.

Piotr Janta has been involved at AP since ‘09 and since ‘15 been a Member of the Management Board. Responsible for the development of sales and marketing communication of the company.

My impression of the culture at Auto Partner that they silently operate and grow the business. People tend to stay long within the organisation and they promote high performers quickly within the organisation. Something I like to see within a business. In an expert interview this what a former branch manager of Auto Partner told.

Of course, I don't even know what position he fills at the moment; I think vice-president, one of the men who started in a sales position, I don't know whether salesman or sales representative. Many of my co-workers, who I also started with, were salesmen at the time when I was a warehouseman, let's say an eye higher in the hierarchy they were already when I came to the company. They are now successful sales directors. One of them is even developing markets outside Poland. So a huge growth, a huge development and the motivation of these people is completely different to people coming in from outside who have already held such a position elsewhere. In my opinion, this builds the company very much. (Former branch manager, Auto Partner SA, August ‘24)

And according to him the mission is clearly defined and both management and employees work well together on it.

Yes, I think the mission has been rather well-known for years, nurtured for years both by the management, cascaded by individual employees. We simply try to supply our customers in the best possible way. It seems to me that here there are no misconceptions or misunderstandings about what we do and why. I think it's very clear and straightforward for every employee. (Former branch manager, Auto Partner SA, August ‘24)

Financials and valuation

We keep the financials section brief, a detailed overview of the financials can be found here in this Google sheets model:

Auto Partner SA financial model

Revenues have been growing with a CAGR of ~25% since ‘15. Net profit grew with a CAGR of ~33% in the same period. Auto Partner (and other distributors) had a tailwind in ‘21- ‘23 due to inflation and rising prices in auto parts. Hence revenue growth has been a bit elevated in that period. Since ‘24 Auto Partner has been dealing with deflation in prices. When I met Piotr, he told me this is still the case.

But volume growth has remained consistent according to management and is growing again this year around +14% to +15%. Inflation is just something they have in control.

Auto Partner dealt with higher wages in Poland and deflation in their prices in ‘24 resulting in pain both on revenues and on expenses. Net profit margin was 5.1% in ‘24. Management believes margins should be able to get back to 6% over time.

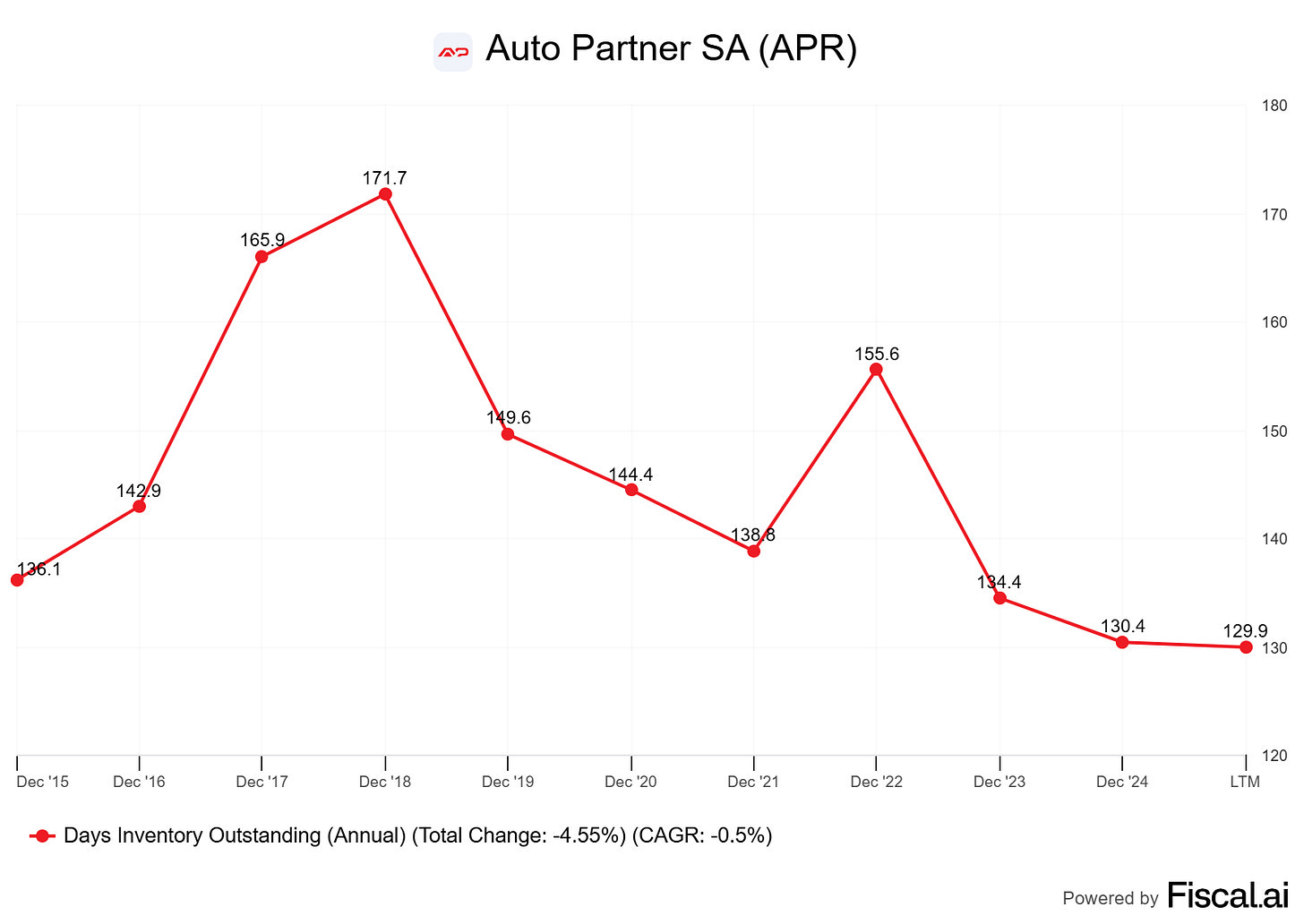

Most of the cash generated is deployed in building larger inventory. Inventory has been growing from zl 435m in ‘18 to zl 1,121m in ‘24. Days of inventory outstanding have slowly been dropping since ‘18.

Typically inventory turnover is low within auto part distributors, especially when you look at the US players, but Auto Partner manages to turn their inventory slightly quicker than its peers. It is something that management is pushing for. They are aware that a lot of cash is tight up in inventory as their inventory grows in line with their revenues. They pay their suppliers on time and probably get discounts for that.

They could easily choose to pay suppliers later and this would free up cash. But as their base currency is the Polish zloty and the suppliers are typically being paid in euro or dollars, swings against euro/dollar could be problematic for Auto Partner.

Net leverage is low (about 1.3x currently) as the company has been repaying debt in ‘23 and ‘24

Valuation

Considering the volumes have been growing about ~15% in the last few years and the fact that they will open a new DC close to Germany, I expect Auto Partner should be able to grow further in the next 5 to 10 years. Nevertheless I keep in my forecast the revenue growth at +12% for the coming five years. I expect AP to reach a net profit margin of 6% over time. If we attach a multiple of 15x, the IRR at current share price is ~21%. At a multiple of 12.5x, IRR would be ~16%. Basically at the current share price, AP should be able to double in 5 years time.

Risks

To make this investment a success, we need the market to consolidate very slowly. If we look at past data, we believe this will remain the case for the next 5-10yrs. If the market consolidates more quickly, it will mean Auto Partner export model will be in danger, as local distributors, wholesalers etc will disappear. EV transition is a risk as the perception is that EVs need less maintenance, but I don’t expect for the next 10yrs this to be a substantial risk for distributors.

Conclusion

I believe Auto Partner is a wonderful business not widely recognized by the broader market. Due to the size of the market cap, larger investors are also not able to buy a stake in the business. At the current valuation, I believe it is set up to produce a decent return in the next five years.

Disclaimer

The information in this article is provided for informational and educational purposes only. The information is not intended to be and does not constitute financial advice or any other advice, is general in nature, and is not specific to you. Before using this article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence. None of the information in this article is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The author is not responsible for any investment decision made by you. You are responsible for your own investment research and investment decisions. The author may or may not have shares of the company.

very insightful deep dive. just sadly, I am also not be to invest in this as well.